WACC vs Hurdle Rate: What's the Difference in Capital Budgeting?

WACC reflects your true cost of capital from markets, while the hurdle rate is management’s higher bar to approve projects, adding a buffer against risk and overoptimism.

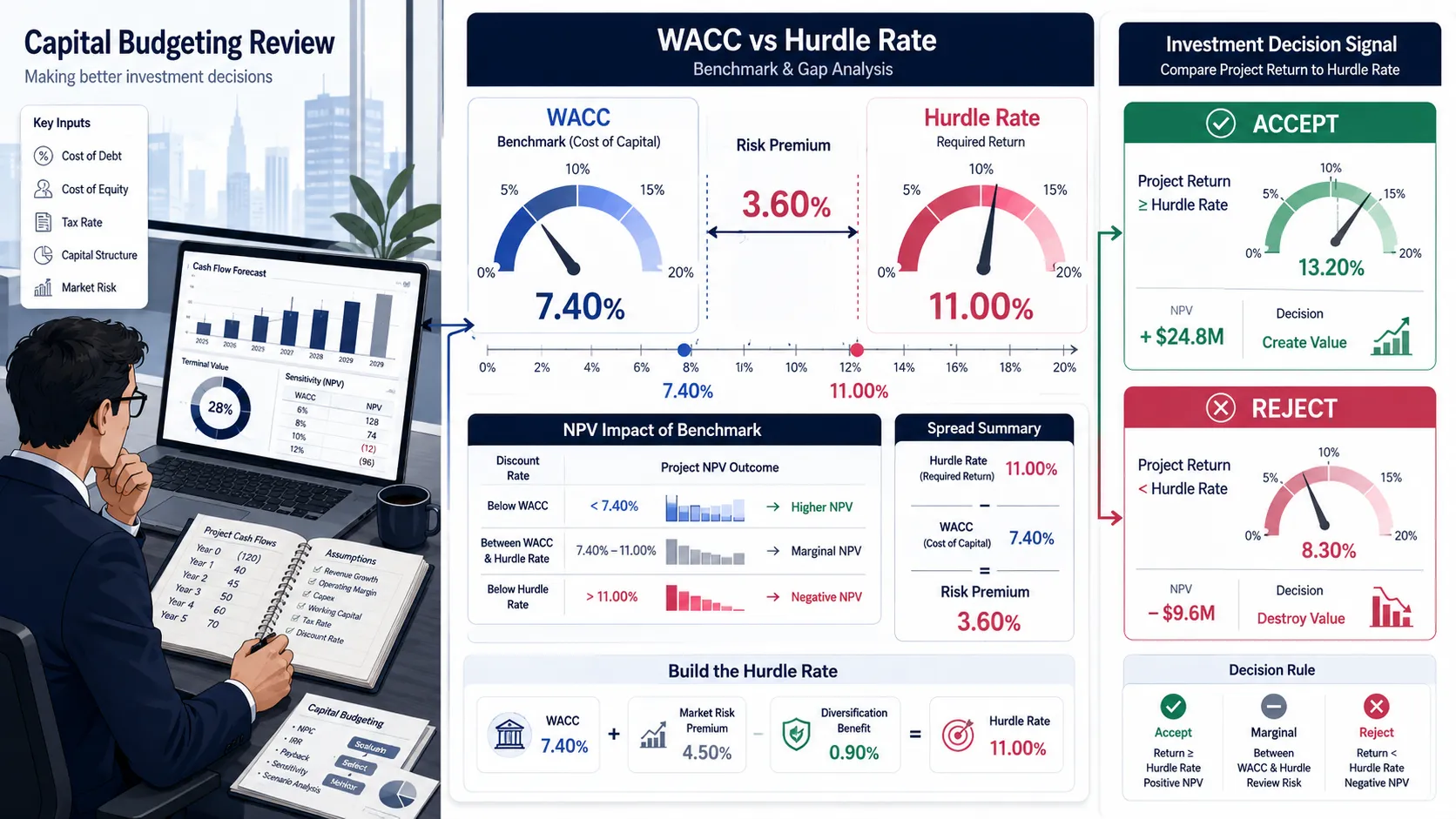

The Short Answer: WACC vs. Hurdle Rate

WACC is the objective cost of raising capital, whereas the Hurdle Rate is the subjective minimum return required to approve a specific project. In corporate finance, a project's Hurdle Rate is almost always equal to or higher than the company's WACC.

Management artificially inflates the WACC to create the Hurdle Rate, building in a buffer against execution risk and optimistic revenue forecasts.

1. What WACC and Hurdle Rate Mean in Finance: The Definitive Answer

Put This Theory into Practice

Calculate WACC step by step using market-value equity and debt weights, CAPM cost of equity, and after-tax cost of debt. Enter your own inputs to model the weighted average cost of capital for any company. Enter your custom inputs and simulate scenarios in our math-verified WACC Calculator.

The short answer is: WACC is a mathematical reality determined by external capital markets, while the Hurdle Rate is an internal management policy. When evaluating a new capital project—such as opening a new factory or acquiring a competitor—management must decide what discount rate to use in their Net Present Value (NPV) calculation.

Using the bare Weighted Average Cost of Capital (WACC) assumes the new project has the exact same risk profile as the company's existing baseline operations.

2026 Hurdle Rate Risk Premium Benchmarks

When setting a hurdle rate, institutional finance teams typically start with the corporate WACC and add a "Risk Premium" based on the project type. Based on 2026 internal capital budgeting standards, here are the typical risk premiums applied:

Project Type | Typical Premium Over WACC | What the Range Usually Signals |

|---|---|---|

Routine Equipment Replacement | +0% to +1% | Identical risk to core business; minimal execution risk. |

Core Market Expansion | +2% to +3% | Moderate sales forecasting risk; requires slight margin of safety. |

New Product Development (R&D) | +5% to +8% | High failure rate; requires massive upside to justify the sunk costs. |

Emerging Market Entry | +7% to +10%+ | Severe geopolitical, currency, and operational execution risks. |

Note: If your company's WACC is 8.0%, an R&D project might face a 15.0% hurdle rate. A project forecasting a 12% IRR would be rejected, even though it technically exceeds the corporate WACC.

Calculate It Yourself: Before you can set a project hurdle rate, you must know your baseline corporate cost of capital. Try our WACC Calculator to lock in your baseline rate instantly.

Why WACC Is Not Always the Correct Hurdle Rate

A common mistake made by non-financial managers is assuming that if the company borrows money at 6% and equity costs 10% (yielding an 8% WACC), any project returning 8.1% should be approved.

This is dangerous for two reasons:

Optimism Bias: Project sponsors notoriously overestimate future cash flows and underestimate costs. Setting a higher hurdle rate acts as a mathematical penalty to offset this optimism.

Capital Rationing: Companies have finite cash. If they have $10M to invest and five projects that all exceed the WACC, they must rank them. The hurdle rate establishes the cut-off line to ensure only the highest-conviction projects receive funding.

Capital Budgeting Red Flag Checklist

When reviewing capital budgeting proposals, watch out for these critical errors regarding discount rates:

Red Flag | Why It Matters |

|---|---|

Using WACC for High-Risk Projects | Discounting a speculative R&D venture at the baseline WACC severely overvalues the project and misallocates capital. |

Hurdle Rate < Cost of Debt | If a project's hurdle rate is lower than the interest rate the company pays to borrow the money to fund it, it guarantees value destruction. |

Inconsistent Discounting | Using a nominal hurdle rate (which includes inflation) to discount real cash flows (which exclude inflation) crushes the NPV. |

Ignoring Project-Specific Debt | If a real estate project is funded entirely by a standalone, non-recourse mortgage, using the blended corporate WACC is mathematically incorrect. |

Sunk Cost Inclusion | Including past R&D spending in the project's cash outflows artificially lowers the IRR and might cause it to fail the hurdle rate unjustly. |

Static Hurdle Rates Across Decades | Using a 15% hurdle rate "because that's what we've always used" ignores the reality of fluctuating macroeconomic interest rates. |

Frequently Asked Questions

Can a hurdle rate be lower than WACC?

In strict financial theory, no. If a project returns less than the WACC, it destroys shareholder value. However, in rare strategic scenarios—such as a "loss leader" project designed to crush a competitor, or a mandatory environmental compliance project required to keep a factory open—management might approve a project with an IRR below the WACC.

They do this knowing it destroys direct financial value to preserve broader enterprise value.

How much of a premium should I add to WACC for a hurdle rate?

It depends entirely on the project's risk profile relative to the company's core operations. For routine maintenance capital expenditures, the premium is often zero. For venturing into unproven markets or high-risk R&D, adding 400 to 800 basis points (4% to 8%) on top of the WACC is standard practice to account for the high probability of failure.

Do venture capital firms use WACC or hurdle rates?

Venture Capital (VC) firms almost exclusively use hurdle rates (often referred to as target IRRs), not WACC. Because early-stage startups have no debt and impossible-to-calculate Betas, standard WACC is useless. VCs typically mandate hurdle rates of 30% to 50% per year to compensate for the reality that 80% of their portfolio companies will fail entirely.

How does inflation impact the hurdle rate?

In 2026, as inflation stabilizes, hurdle rates must remain aligned with nominal expectations. A company's WACC is inherently nominal (it includes inflation expectations built into the risk-free rate). Therefore, the hurdle rate is also nominal.

You must ensure that the cash flows you are forecasting also include projected price increases (inflation) to maintain mathematical consistency.

Should I use the hurdle rate for my NPV calculation?

Yes. When running an NPV analysis for a specific high-risk project, you should discount the projected free cash flows using the risk-adjusted hurdle rate, not the baseline corporate WACC. Doing so ensures your Net Present Value accurately reflects the specific execution risks of that project. You can run this analysis using our NPV Calculator.

What happens if IRR equals the hurdle rate?

If a project's Internal Rate of Return (IRR) exactly equals the hurdle rate, its Net Present Value (NPV) is exactly zero (when discounted at the hurdle rate). In capital budgeting theory, this means the project is "acceptable" because it meets the minimum required return, but it does not generate any excess value beyond the required risk premium.

Put This Theory Into Practice

Run your own scenario analysis with our math-verified calculators.