What Is After-Tax Cost of Debt and How Does It Lower WACC?

Interest payments are tax-deductible, making debt cheaper than equity and lowering your company's WACC. The after-tax cost of debt reveals this true, subsidized borrowing rate.

The Short Answer: After-Tax Cost of Debt

The after-tax cost of debt is the true, out-of-pocket interest rate a company pays on its borrowings after accounting for tax deductions.

Formula:

After-Tax Rd = Pre-Tax Rd × (1 - Tax Rate)Because interest payments are tax-deductible in the U.S. and most developed economies, the government effectively subsidizes corporate debt. This makes debt significantly cheaper than equity, incentivizing companies to borrow money and actively lowering their overall Weighted Average Cost of Capital (WACC).

1. What After-Tax Cost of Debt Means in Finance: The Definitive Answer

Put This Theory into Practice

Determine risk-adjusted discount rates with market weights, CAPM equity cost, and tax-shielded debt. Enter your custom inputs and simulate scenarios in our math-verified WACC Calculator.

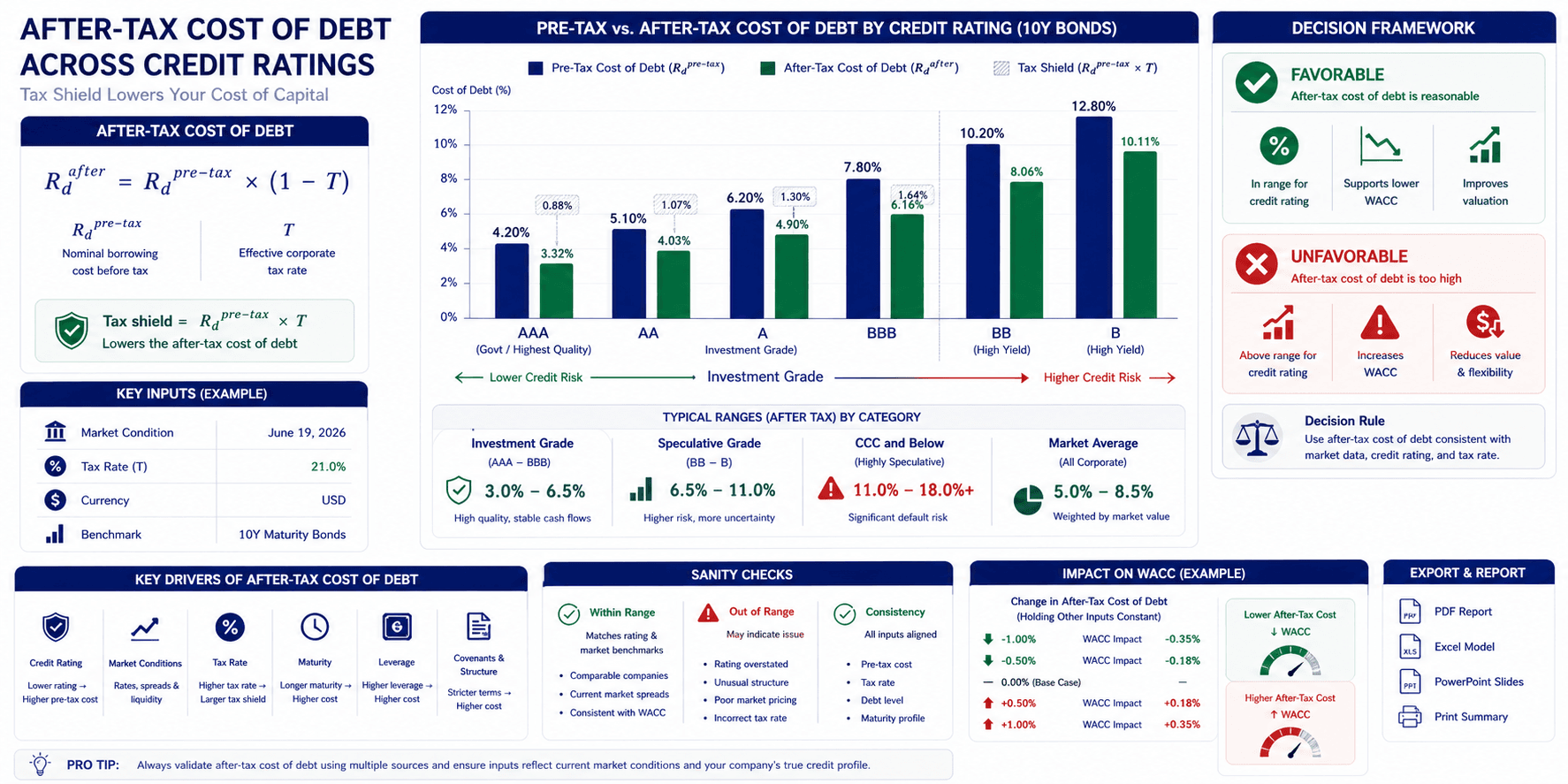

The short answer is: the tax shield on debt fundamentally alters corporate valuation. When building a WACC model, you cannot simply take the interest rate a company pays the bank and plug it into your formula. If a company issues bonds at a 6.0% yield, but has a 25% corporate tax rate, the tax savings offset a quarter of the interest expense.

The true cost borne by the company is only 4.5%. This is the exact rate you must use in your WACC calculation.

2026 Corporate Debt Benchmarks (Pre-Tax vs After-Tax)

To contextualize the power of the tax shield, consider the 2026 corporate bond market. Assuming a standard 25% effective tax rate, here is how the tax shield compresses the true cost of debt across different credit ratings:

Credit Rating (Risk) | Typical Pre-Tax Yield | After-Tax Cost (25% Tax Rate) | What the Range Signals |

|---|---|---|---|

AAA / AA (Prime) | 4.8% – 5.2% | 3.6% – 3.9% | Elite balance sheets; debt is nearly as cheap as inflation. |

BBB (Investment Grade) | 5.8% – 6.5% | 4.3% – 4.9% | The standard corporate borrower; healthy tax shield utilization. |

BB / B (High Yield/Junk) | 8.0% – 10.5% | 6.0% – 7.9% | High default risk; even with the tax shield, capital is expensive. |

Note: If your calculated after-tax cost of debt exceeds your Cost of Equity (CAPM), your model is fundamentally broken. Debt is senior to equity and must always be cheaper.

Calculate It Yourself: Don't calculate these tax shields by hand. Use our WACC Calculator to enter your Pre-Tax Cost of Debt and Tax Rate, and let the engine automatically apply the tax shield to your final discount rate.

Why the Tax Shield Drives Capital Structure Decisions

The after-tax cost of debt is the primary reason companies do not fund themselves with 100% equity. Equity is expensive (investors demand high returns for high risk) and dividends paid to shareholders are not tax-deductible.

By replacing expensive equity with cheap, tax-deductible debt, a CFO can immediately lower the company's WACC. A lower WACC increases the Net Present Value of future cash flows, driving the stock price higher. However, this only works up to a certain point.

If management takes on too much debt, the rising risk of bankruptcy causes both the cost of debt and the cost of equity to skyrocket, erasing the benefits of the tax shield.

Cost of Debt Modeling Red Flag Checklist

When auditing a WACC model or DCF, watch out for these critical errors regarding the cost of debt:

Red Flag | Why It Matters |

|---|---|

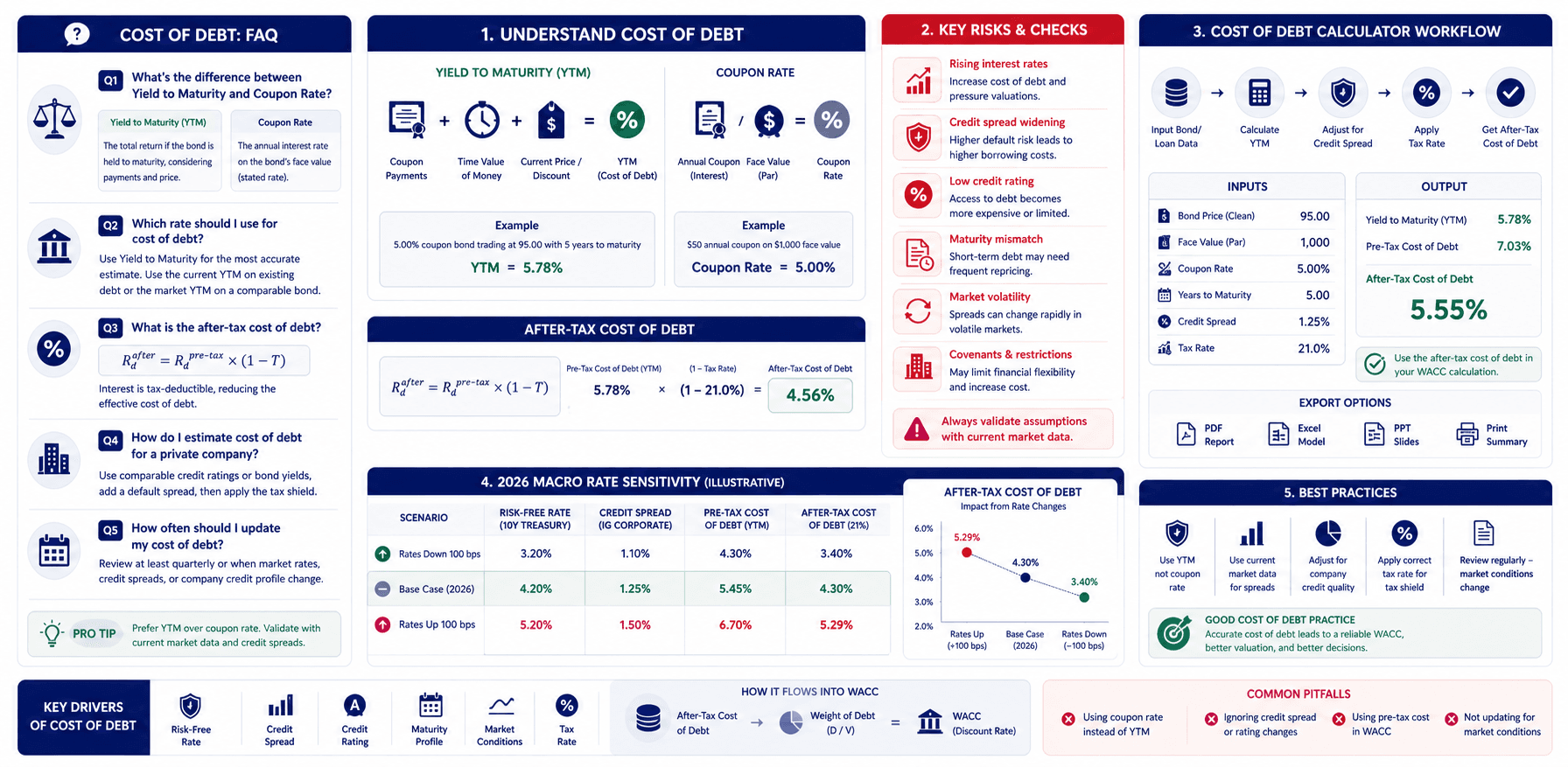

Using Coupon Rate Instead of Yield to Maturity (YTM) | The coupon rate is historical (what the bond paid when issued). YTM is the forward-looking market rate today. You must use YTM. |

Forgetting the Tax Shield Entirely | Plugging the pre-tax cost of debt directly into the WACC formula mathematically overstates the discount rate and undervalues the company. |

Using Statutory Instead of Effective Tax Rates | The 21% U.S. Federal statutory rate ignores state, local, and foreign taxes. Always use the company's blended effective or marginal tax rate from its 10-K. |

Applying Tax Shields to Loss-Making Startups | If a company has massive net operating losses (NOLs) and pays zero taxes, its tax rate is 0%. The after-tax cost equals the pre-tax cost. |

Calculating Debt Cost from Book Values | Interest expense divided by total book debt yields a historical, blended rate. It fails to capture the current market cost of raising new debt in 2026. |

Frequently Asked Questions

Should I use the coupon rate or yield to maturity?

You must use Yield to Maturity (YTM). The WACC is a forward-looking metric used to discount future cash flows. The coupon rate only tells you what the interest rate environment was five years ago when the bond was issued. YTM tells you exactly what the market demands to lend the company new money today.

What if a company operates at a net loss?

If a company is unprofitable and generating Net Operating Losses (NOLs), it is not paying income taxes. Therefore, it cannot immediately utilize the interest tax deduction. In this scenario, the effective tax rate is 0%, meaning the after-tax cost of debt is exactly equal to the pre-tax cost of debt.

(Note: In advanced modeling, analysts sometimes forecast a future normalized tax rate once the company turns profitable).

Do I use the marginal or effective tax rate?

In rigorous academic finance, the marginal tax rate is preferred because it represents the tax savings on the next dollar of debt issued. However, in practical institutional modeling, analysts frequently use the effective tax rate (Total Tax Expense / Pre-Tax Income) from the company's recent 10-K filings, as it provides a blended reality of the company's global tax liabilities.

Why isn't there an after-tax cost of equity?

The tax code treats debt and equity differently. Interest payments made to bondholders are classified as a business expense and are therefore tax-deductible before net income is calculated. Dividends paid to equity shareholders are paid out of net income, after corporate taxes have already been levied.

Because equity payouts provide no corporate tax relief, there is no "tax shield" for equity.

How do 2026 interest rate hikes affect the tax shield?

When macroeconomic interest rates rise, a company's pre-tax cost of debt increases. Mathematically, a higher interest expense means a larger absolute tax deduction. However, the relative benefit of the tax shield remains constant (it is fixed to the corporate tax rate).

Despite the larger dollar-value tax deduction, the overall after-tax cost of debt will still be significantly higher in a high-rate environment, driving up the company's WACC.

Does preferred stock get the same tax treatment as debt?

No. Preferred stock acts like a hybrid between debt and equity, paying a fixed dividend similar to a bond's coupon. However, legally, it is equity. Preferred dividends are not tax-deductible. Therefore, the cost of preferred stock in the WACC formula is calculated on a purely pre-tax basis.

Put This Theory Into Practice

Run your own scenario analysis with our math-verified calculators.