DCF Calculator: Discounted Cash Flow Valuation Model

Use this DCF calculator to estimate enterprise value, equity value, terminal value, and per-share value from projected free cash flow, WACC, terminal growth, exit multiple, net debt, and share count assumptions.

Before running a DCF, you need a discount rate. For unlevered free cash flow models, this is typically the Weighted Average Cost of Capital (WACC). The model supports multi-year free cash flow forecasts, WACC or discount rate assumptions, perpetual growth terminal value, net debt adjustments, and fully diluted share counts.

Have a suggestion or found a calculation discrepancy? Let us know!

How to Build a DCF Valuation

Choose quick growth or year-by-year cash flows

Under Quick Growth mode, input starting Free Cash Flow (FCF) and a constant growth rate. The calculator will project FCFs automatically over 5-10 years. Under Year-by-Year mode, input custom FCF values for each individual forecast period to model fluctuating revenues.

Select a discount rate and terminal value method

Input a discount rate (typically WACC). Select Perpetuity Growth (Gordon Growth) to model infinite growth (typically 2%-3% long-term inflation rate), or Exit Multiple to assume the business is sold in the final year at a multiple of EBITDA, Revenue, or FCF.

Enter net debt and shares outstanding

To transition from Enterprise Value to Equity Value, input Net Debt (Total Debt minus Cash & Equivalents). Input preferred stock and minority interests if applicable. Provide total shares outstanding to compute the final intrinsic implied share price.

DCF Scenario Analysis

Change cash flow assumptions by scenario

Valuation is highly sensitive to forecasts. By calculating Bull (optimistic), Base (moderate), and Bear (pessimistic) assumptions, you avoid single-point estimates. Adjust annual growth, margins, and discount rates across scenarios to see the range of corporate value.

Compare enterprise and equity value ranges

Comparing scenario outputs maps your company's potential valuation spread. A wide gap between Bear and Bull highlights high risk or execution sensitivity, while a tight spread represents business stability and cash flow predictability.

Save, copy, and restore scenarios

Log in to save multiple scenario snapshots directly to your workspace. Clone current configurations to create bull/bear adjustments without rekeying baseline inputs, and restore previous calculation snapshots from your history ledger.

DCF Sensitivity Analysis

Discount rate and terminal growth matrix

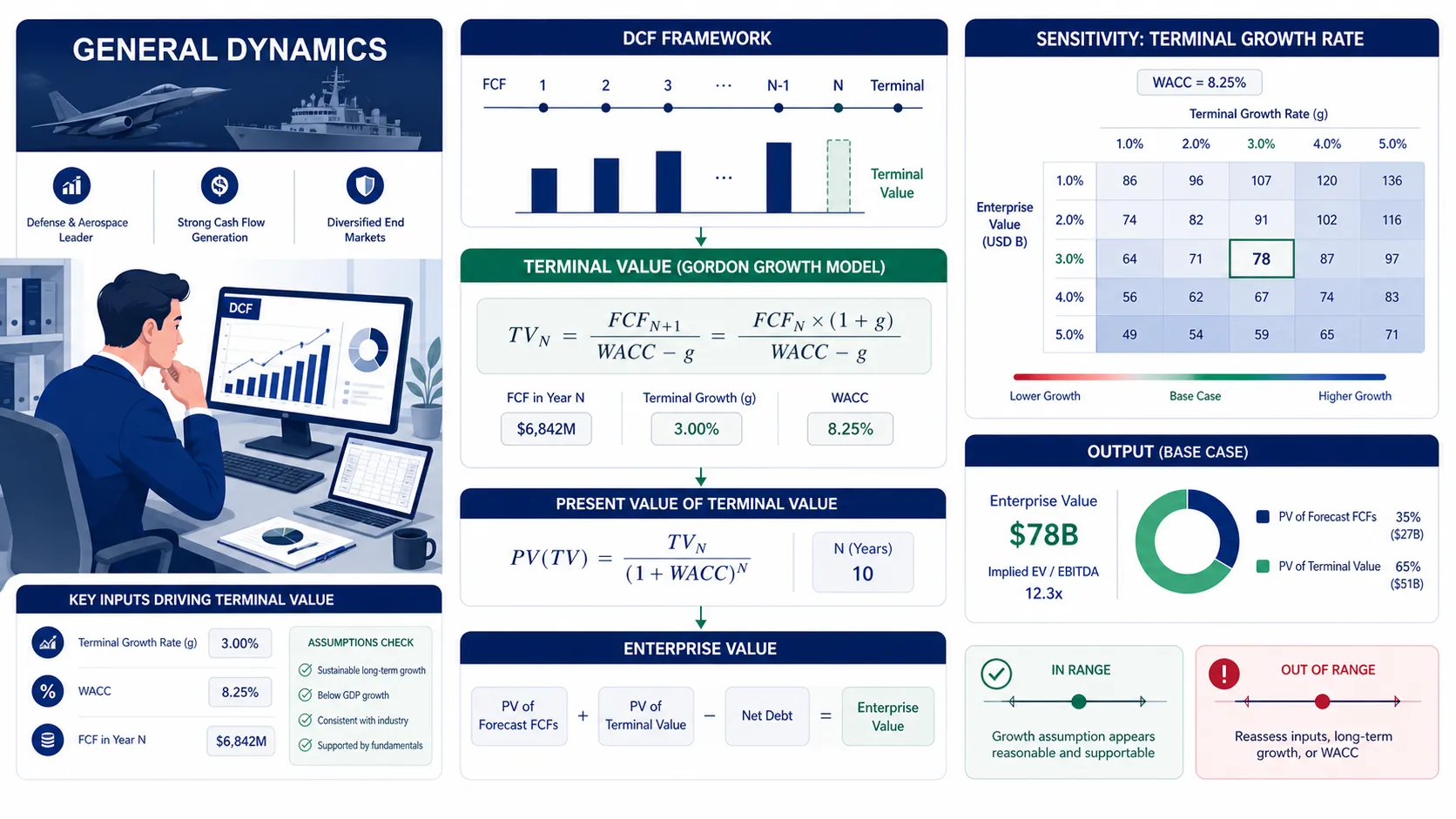

The 5x5 sensitivity matrix automatically cross-references the Hurdle Discount Rate against the Perpetual Growth Rate. This grids WACC adjustments (vertical) against perpetual terminal value growth (horizontal), calculating the implied per-share value of each intersection.

Discount rate and exit multiple matrix

When using the Exit Multiple method, the matrix swaps the growth axis for the exit multiple axis (e.g., 8x to 12x EBITDA). This helps corporate transaction leads determine fair transaction spreads and valuation hurdles under different acquisition multiples.

How to interpret invalid sensitivity cells

In perpetuity growth, WACC must be strictly greater than the terminal growth rate (WACC > g). If the discount rate is equal to or less than growth, the denominator is zero or negative, yielding an infinite valuation. The matrix labels these cells as "N/A" to ensure modeling logic safety.

DCF Formula

Present Value of FCF

Each period cash flow is discounted using compounding discount factors:

Perpetuity growth terminal value

The Gordon Growth model values the business beyond the forecast period using a steady perpetual growth rate:Terminal Value = FCF_n * (1 + g) / (r - g)This method assumes the business grows at rate (g) forever. The perpetual growth rate must be lower than the long-term economic GDP growth rate.

Exit multiple terminal value

The Exit Multiple method assumes the company is sold to a strategic buyer in the final forecast year:Terminal Value = Terminal Metric * Exit MultipleCommon metrics include EBITDA, Revenue, or final year FCF. Multiples are benchmarked against actual market transactions of comparable listed peers.

FCF Forecast Assumptions

Revenue growth

A DCF forecast usually starts with revenue growth. Growth should slow toward a sustainable long-term rate as the company matures, unless the model explicitly supports a temporary expansion phase.

Margin and reinvestment

Free cash flow depends on operating margin, taxes, capital expenditures, depreciation, and working capital. Strong revenue growth can still produce weak FCF if reinvestment needs are heavy.

Forecast length

Five to ten years is common for explicit forecasts. The forecast period should be long enough for the business to approach a normalized margin and growth profile before terminal value begins.

Terminal Value: Gordon Growth vs Exit Multiple

Gordon Growth method

Gordon Growth estimates terminal value from normalized final-year free cash flow, perpetual growth, and discount rate. It is internally consistent with cash flow fundamentals but highly sensitive to the spread between WACC and growth.

Exit multiple method

Exit multiple valuation applies a market multiple to a terminal metric such as EBITDA, revenue, or FCF. It is easier to benchmark against comparable companies but can import market-cycle assumptions into the model.

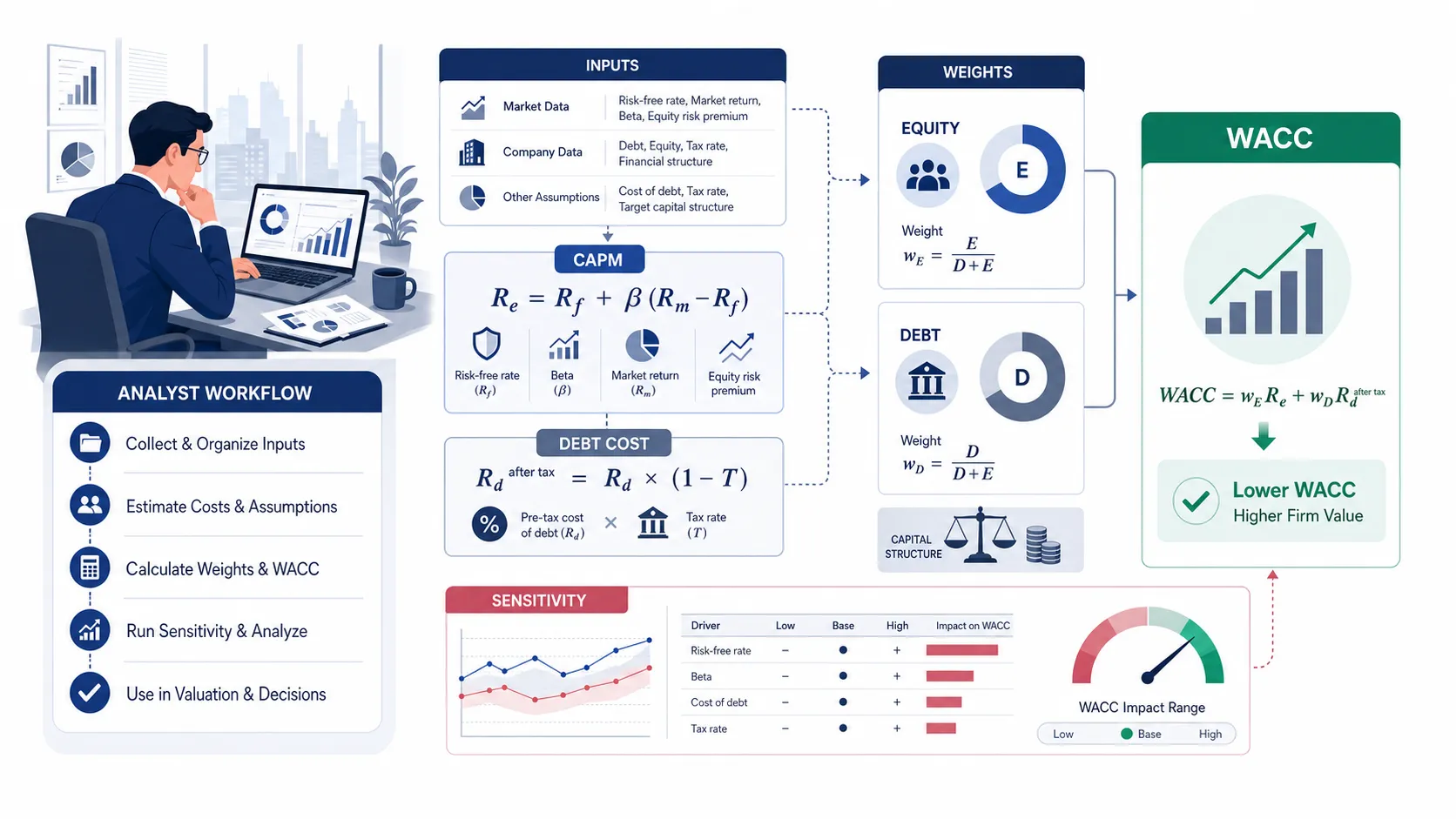

Discount Rate and WACC in DCF Models

Use WACC for unlevered FCF

If the DCF uses unlevered free cash flow, WACC is commonly used because the cash flows belong to all providers of capital before debt payments.

Match risk to cash flow

A higher-risk project, country, or early-stage company may require a higher discount rate than a mature company-wide WACC.

Check the value impact

DCF value can move sharply when WACC changes by even one percentage point, especially when terminal value is a large portion of enterprise value.

DCF Assumption Changes: Terminal Growth and Discount Rate

Terminal growth assumption changes

Terminal growth assumptions change when long-term inflation, industry maturity, reinvestment needs, market share limits, or competitive pressure change. A mature company with stable cash flow may support a lower, economy-like perpetual growth rate, while a company facing margin compression or shrinking demand may require a more conservative terminal growth assumption.

In a DCF model, terminal growth should normally remain below the discount rate and should be consistent with the company's long-term addressable market. Small changes can move enterprise value sharply because terminal value often represents a large share of total DCF value.

Discount rate assumption changes

Discount rate or WACC assumptions change when interest rates, credit spreads, equity risk premiums, leverage, beta, country risk, or company-specific risk change. A higher discount rate reduces the present value of future cash flows, while a lower rate increases present value.

Analysts should refresh WACC assumptions when a company issues debt, changes its capital structure, enters a riskier market, or faces a major shift in operating volatility. This calculator is an educational model, so assumption changes should be documented and sensitivity-tested rather than treated as investment advice.

From enterprise value to equity value

Subtracting net debt

Enterprise Value (EV) measures the value of corporate operations. To isolate value attributable to stock shareholders, we deduct corporate debt and add back surplus cash. This is formulated as deducting Net Debt (Total Debt minus Cash & Equivalents).

Adding non-operating adjustments

In corporate structures, non-operating assets (such as non-consolidated equity stakes, idle real estate assets, or treasury securities) must be added back to build an accurate bridge, while preferred stocks and minority interests are subtracted.

Calculating value per share

Once Equity Value is derived, divide it by the total outstanding common shares. This yields the intrinsic value per share. Comparing this intrinsic share price to the current market trading price highlights potential overvaluation or undervaluation.

DCF example calculation

Example cash flow assumptions

Let's evaluate a business with a starting Year 0 FCF of $100,000, growing at 8.00% annually for 5 years, with a discount rate (WACC) of 10.00%, and a perpetual growth rate (g) of 3.00%. Net debt is $200,000, and shares are 1,000,000.

Step-by-step present value calculation

Project Year 1-5 cash flows: $108,000; $116,640; $125,971; $136,049; $146,933. Discounting each yields the Present Value of Cash Flows: Sum of PV(FCFs) = $473,379.

Terminal value and valuation bridge

Terminal Value = $146,933 * 1.03 / (0.10 - 0.03) = $2,162,011. PV of Terminal Value is $1,342,439. Summing these yields an Enterprise Value (EV) of $1,815,818. Deducting Net Debt of $200,000 leaves an Equity Value of $1,615,818. Value per share is $1.62.

What your DCF result means

Why DCF produces a valuation range

A DCF does not produce a singular absolute figure; it generates a range of values. Because slight shifts in cash flows or rates cause wide valuations, analysts use a sensitivity matrix to establish floor and ceiling thresholds for investment margins of safety.

How WACC changes present value

WACC serves as the hurdle multiplier. A higher WACC lowers the present value of distant cash flows because of interest compounding. Companies with stable revenues enjoy lower WACCs, preserving remote cash flow values.

Why terminal value concentration matters

If over 70% of enterprise value rests on the Terminal Value, the valuation is heavily reliant on distant assumptions rather than immediate operations. A high TV concentration indicates elevated investment risk and a need to test exit assumptions carefully.

DCF use cases for SaaS, private companies, and small businesses

SaaS free cash flow assumptions

SaaS models feature deferred cash revenues and high upfront customer acquisition costs (CAC). Standard EBITDA models fail to capture cash dynamics. Projections rely on customer lifetime value (LTV), churn rates, and growth margins to compute true cash profiles.

Private company discount-rate limitations

Private companies lack publicly observable stock betas. To derive the appropriate discount rate, analysts compile public peers, calculate their average asset beta, and relever that benchmark to the private firm's debt-to-equity ratios.

Small business normalization adjustments

Small business statements contain non-operating expenditures or owner-operator salary anomalies. Before modeling FCFs, adjust accounting records to state normalized earnings as if a professional third-party manager were running operations.

- Levered vs. Unlevered cash flows: Mixing levered cash flows with WACC (unlevered discount rate), which double-counts interest benefits.

- Inconsistent discount rates: Changing the discount rate annually without factoring in capital structure transitions.

- Terminal growth rate anomaly: Setting perpetuity growth (g) higher than long-term GDP inflation rate (typically > 3.5%).

- Double-counting assets: Leaving cash balance in adjustments while it is already included in Net Debt deductions.

Real-world case study: Apple Inc. (AAPL, FY 2023)

Apple Inc. metrics profile

Apple Inc. (AAPL) is a global technology leader, and its robust financial performance makes it a prime candidate for a Discounted Cash Flow (DCF) valuation. Analyzing its recent financial data provides insights into its cash-generating capabilities and future growth prospects, essential for investors to assess its intrinsic value.

Apple's substantial Free Cash Flow of $99.584 billion in FY 2023 highlights its strong operational efficiency and ability to generate significant cash after accounting for operating expenses and capital investments. This cash flow, combined with a projected revenue growth rate of 8%, an effective tax rate of 14.7%, and a WACC of 8.35%, forms the critical basis for a Discounted Cash Flow valuation. A DCF analysis for Apple would involve projecting these cash flows into the future, discounting them back to the present using the WACC, and adding a terminal value based on the long-term growth assumption. This approach helps investors determine the intrinsic value of Apple's stock, providing a fundamental perspective beyond market price fluctuations.

Related Calculators

Estimate weighted average cost of capital.

Open Tool →NPV CalculatorCompute net present value of cash flows.

Open Tool →IRR CalculatorSolve project internal rates of return.

Open Tool →Free Cash Flow CalculatorEstimate operating free cash flow.

Open Tool →Break-Even ROI CalculatorAnalyze payback thresholds and returns.

Open Tool →EBITDA Margin CalculatorAssess earnings margin before interest and tax.

Open Tool →Related Articles & Guides

Corporate Finance

Corporate FinanceTerminal Growth Rate Changes: How They Impact DCF Valuation Models

A 0.5% shift in terminal growth rate can swing DCF valuation by 15%, as terminal value often drives over 70% of enterprise worth. CFOs must cap perpetuity growth at GDP or risk-free rates to avoid model distortions.

Corporate Finance

Corporate FinanceHow to Calculate WACC: The Complete Step-by-Step Formula for Corporate Valuation

A 100-basis-point WACC error can swing a $500M valuation by $40–80M. This guide delivers the exact formula and five critical inputs corporate operators need to get the discount rate right.

Corporate Finance

Corporate FinanceWACC by Industry: 2026 Benchmarks for Technology, Healthcare, and Real Estate

In 2026, industry WACC diverges sharply, from 5.5% for utilities to over 11.5% for software. CFOs must benchmark their discount rate against peers to ground valuations in market reality.

Frequently Asked Questions

What discount rate should I use in a DCF calculator?

How many projection years should a DCF use?

Should I use perpetuity growth or an exit multiple?

Why does terminal value dominate some DCF models?

Can a DCF produce a negative equity value?

Is a DCF result an investment recommendation?

The calculations, projections, and reports generated by BizToolkitPro are for educational and informational purposes only. They do not represent professional investment advice, financial planning, tax guidance, legal counsel, or formal business valuation.

Financial models and valuation formulas (including WACC, DCF, IRR, and NPV) rely on assumptions and inputs provided directly by the user. Actual financial markets and business metrics fluctuate; therefore, BizToolkitPro makes no warranties, express or implied, regarding the accuracy, completeness, or suitability of the outputs for any investment strategy or corporate decision.

Always perform your own independent diligence and consult with a licensed Financial Analyst, Certified Public Accountant (CPA), or certified valuation specialist before committing capital or executing corporate transactions.