How to Find Beta for WACC: Unlevered vs Levered Beta Calculati

Unlock institutional-grade WACC by mastering bottom-up beta: unlever public peers to strip debt risk, then re-lever for your target's capital structure. This precision method solves CAPM's toughest hurdle, delivering accurate equity risk pricing for DCF models.

Featured Workflow: Calculating Bottom-Up Beta

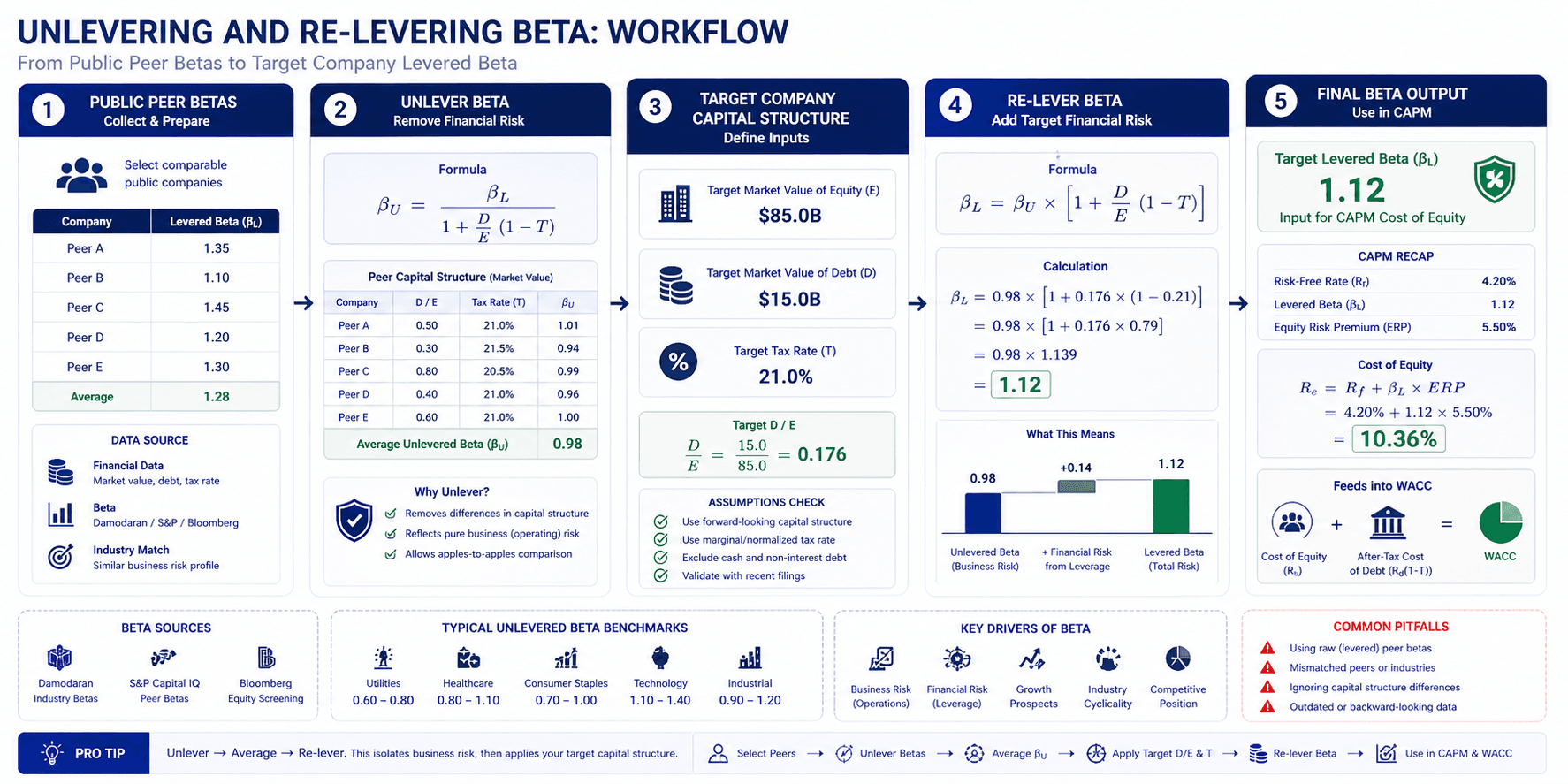

For private companies, calculate Beta by unlevering public peers to remove their debt risk:

`Unlevered Beta = Levered Beta / [1 + (1 - Tax Rate) × (Debt / Equity)]`Then, "re-lever" that result using your target company's specific capital structure. This generates an institutional-grade Levered Beta that accurately prices equity risk for your WACC and DCF models.

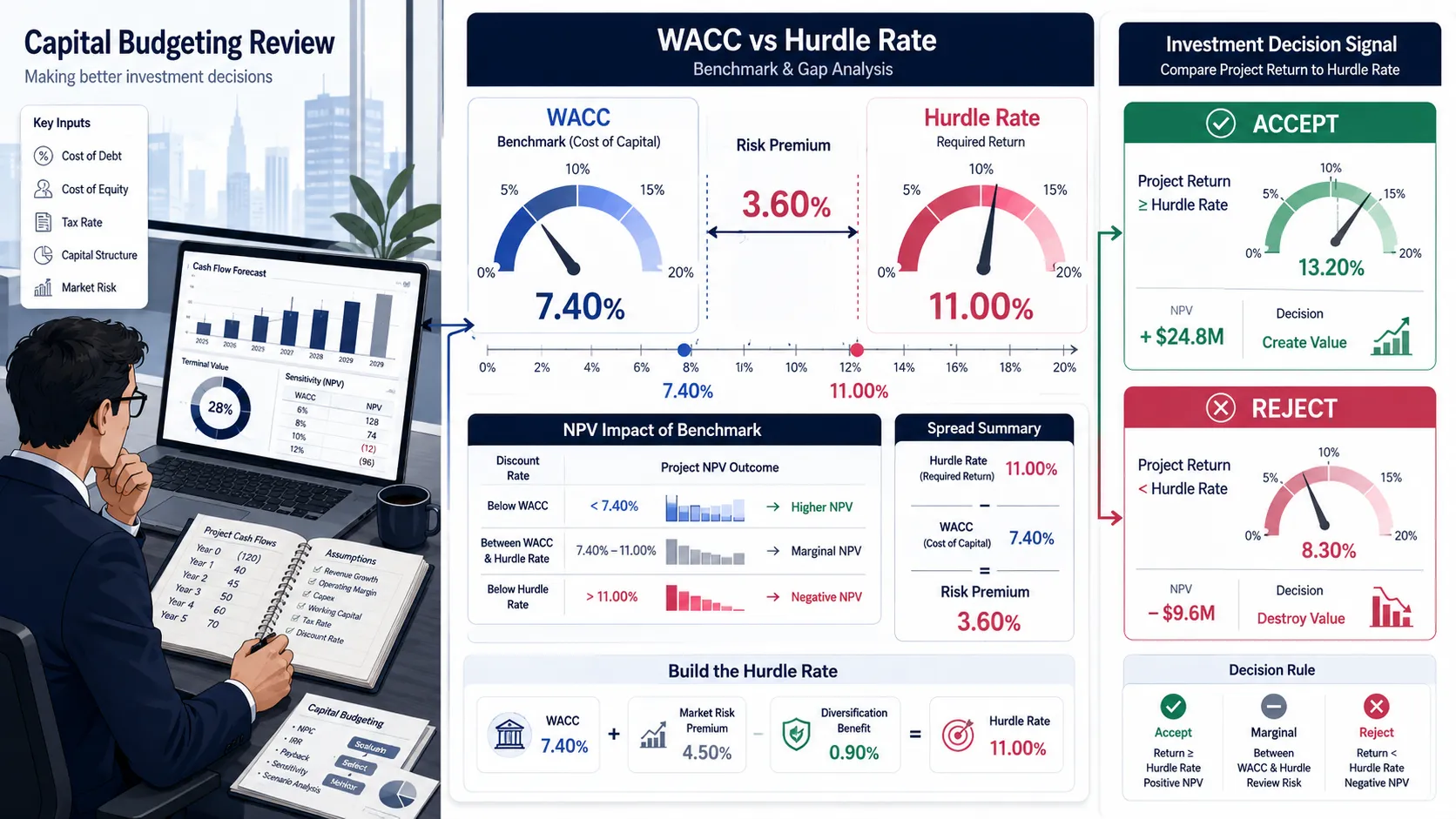

When calculating the Weighted Average Cost of Capital (WACC), the cost of debt is observable, and the risk-free rate is posted daily by the Treasury. However, determining the cost of equity requires solving for Beta ($\beta$)—a measure of how violently a stock moves relative to the broader market.

Knowing exactly how to find Beta for WACC is the most complex hurdle in the CAPM formula, especially when valuing private companies that have no publicly traded stock.

Put This Theory into Practice

Determine risk-adjusted discount rates with market weights, CAPM equity cost, and tax-shielded debt. Enter your custom inputs and simulate scenarios in our math-verified WACC Calculator.

1. Understanding Beta in Corporate Finance

Beta measures systematic risk. A Beta of 1.0 means the company moves perfectly in tandem with the S&P 500. A Beta of 1.5 indicates it is 50% more volatile, demanding a higher return from equity investors. However, there are two distinct types of Beta: Levered and Unlevered.

Levered vs Unlevered Beta: The Core Formulas

Levered Beta ($\beta_L$): This is the raw number you see on Yahoo Finance or a Bloomberg Terminal. It includes both the core business risk (making the product) and the financial risk generated by the company's specific debt load. You must use Levered Beta in the CAPM formula.

Unlevered Beta ($\beta_U$): This represents the pure operational risk of the business, pretending the company has zero debt.

To convert between the two, analysts use the Hamada Equation:

Input for Unlevering | Source | Example (FY2026) |

|---|---|---|

Levered Beta ($\beta_L$) | Peer Company Public Data | 1.30 |

Debt/Equity Ratio ($D/E$) | Peer Company Capital Structure | 0.40 |

Marginal Tax Rate ($T$) | Statutory Corporate Rate | 25.0% |

Unlevered Beta = Levered Beta / [1 + (1 - T) × (D/E)]

Common Beta Modeling Mistakes

Beta is the most frequently manipulated variable in corporate valuation. Avoid these critical modeling errors:

Plugging Unlevered Beta directly into CAPM: Unlevered Beta strips out the risk of debt. Because equity shareholders bear the brunt of bankruptcy risk, using Unlevered Beta in CAPM artificially suppresses the cost of equity and massively overvalues the company.

Using Raw Regression Beta: Raw Betas generated by standard statistical regression contain high standard errors. Institutional analysts always use "Adjusted Beta" (smoothing the raw Beta toward 1.0) to account for mean reversion over time.

Mismatched Peer Sets: Unlevering the Beta of a mature, dividend-paying software giant (like Oracle) to re-lever for a hyper-growth, cash-burning AI startup. The operational risk profiles are fundamentally incompatible.

Book vs. Market D/E Ratios: When unlevering peer Betas, you must use the market value of equity for the $D/E$ ratio, not the book value from the balance sheet.

The Gold Standard Data Source: Damodaran

Instead of manually unlevering 50 peer companies, institutional analysts rely on Professor Aswath Damodaran at NYU Stern. His free datasets provide pre-calculated average Unlevered Betas for nearly 100 specific industries globally, updated annually. In 2026, pulling an industry Unlevered Beta directly from Damodaran is the industry standard for private company valuation.

💡 Pro Tip: Once you have calculated your final Levered Beta, you can instantly generate your Cost of Equity. Use our WACC Calculator — input your Beta and capital structure, and the engine handles the rest.

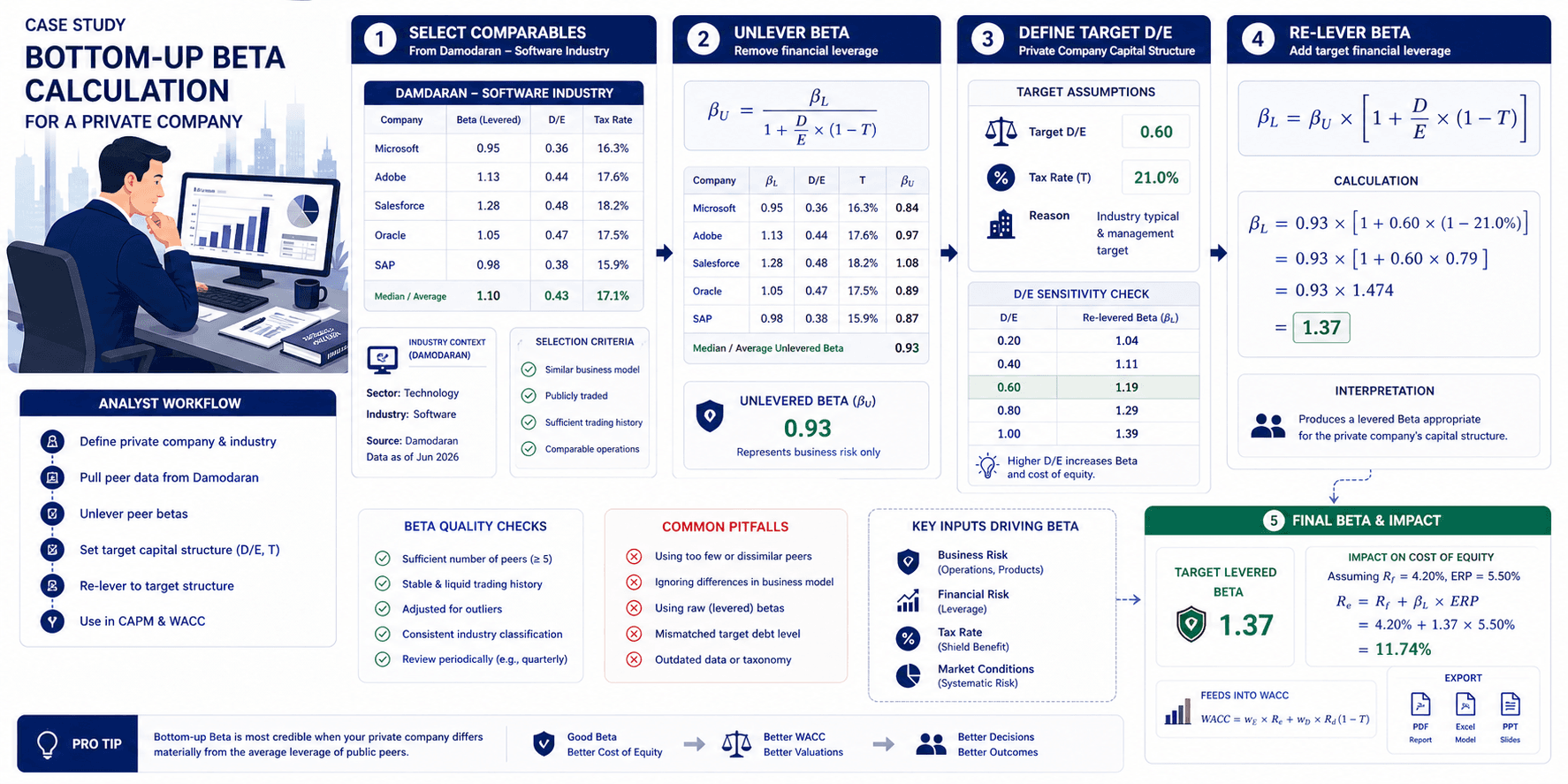

2. Deep Case Study: Finding Beta for a Private SaaS Company

This case study uses illustrative SaaS industry metrics and market assumptions appropriate for a FY2026 valuation date. It is an educational modeling example.

Assume you are valuing "CloudMetrics Inc.", a rapidly growing, privately held B2B SaaS company preparing for an acquisition. Because CloudMetrics is private, it has no stock price and therefore no raw Levered Beta. We must build a Bottom-Up Beta.

Quick Bottom-Up Beta Example: The 30-Second Version

Here is the fast-track logic:

Step 1: The Software industry's average Unlevered Beta is 1.10.

Step 2: CloudMetrics plans to operate with a target capital structure of 20% Debt and 80% Equity ($D/E = 0.25$), with a 21% Tax Rate.

Step 3: Re-lever the industry Beta:

Levered Beta = 1.10 × [1 + (1 - 0.21) × 0.25]=1.10 × 1.1975= 1.32

Unlevering the Software Industry Peers

In a full institutional model, rather than taking a broad industry average, you curate a specific peer group of 5 to 8 publicly traded SaaS companies that closely match CloudMetrics' revenue model.

Assume the median Levered Beta of this peer group is 1.45. However, these public peers carry heavy debt loads, with a median Debt-to-Equity ($D/E$) ratio of 0.60 and an effective tax rate of 25%.

We must first strip out the peers' debt risk to find the pure operational risk (Unlevered Beta):

Unlevered Beta = 1.45 / [1 + (1 - 0.25) × 0.60]Unlevered Beta = 1.45 / [1 + 0.45]Unlevered Beta = 1.45 / 1.45= 1.00

The pure operational risk of selling this type of software is 1.00.

Re-levering for the Private Target

Now we apply CloudMetrics' specific financial risk. CloudMetrics is funded mostly by venture capital, with very little debt. Its target $D/E$ ratio is only 0.15, with a 21% tax rate.

We re-lever the pure operational Beta (1.00) using CloudMetrics' specific debt load:

Target Levered Beta = 1.00 × [1 + (1 - 0.21) × 0.15]Target Levered Beta = 1.00 × [1 + 0.1185]= 1.12

Because CloudMetrics carries significantly less debt than its public peers, its final Levered Beta (1.12) is much lower than the peer median (1.45). This 1.12 is the exact number you will plug into the CAPM formula to find CloudMetrics' cost of equity.

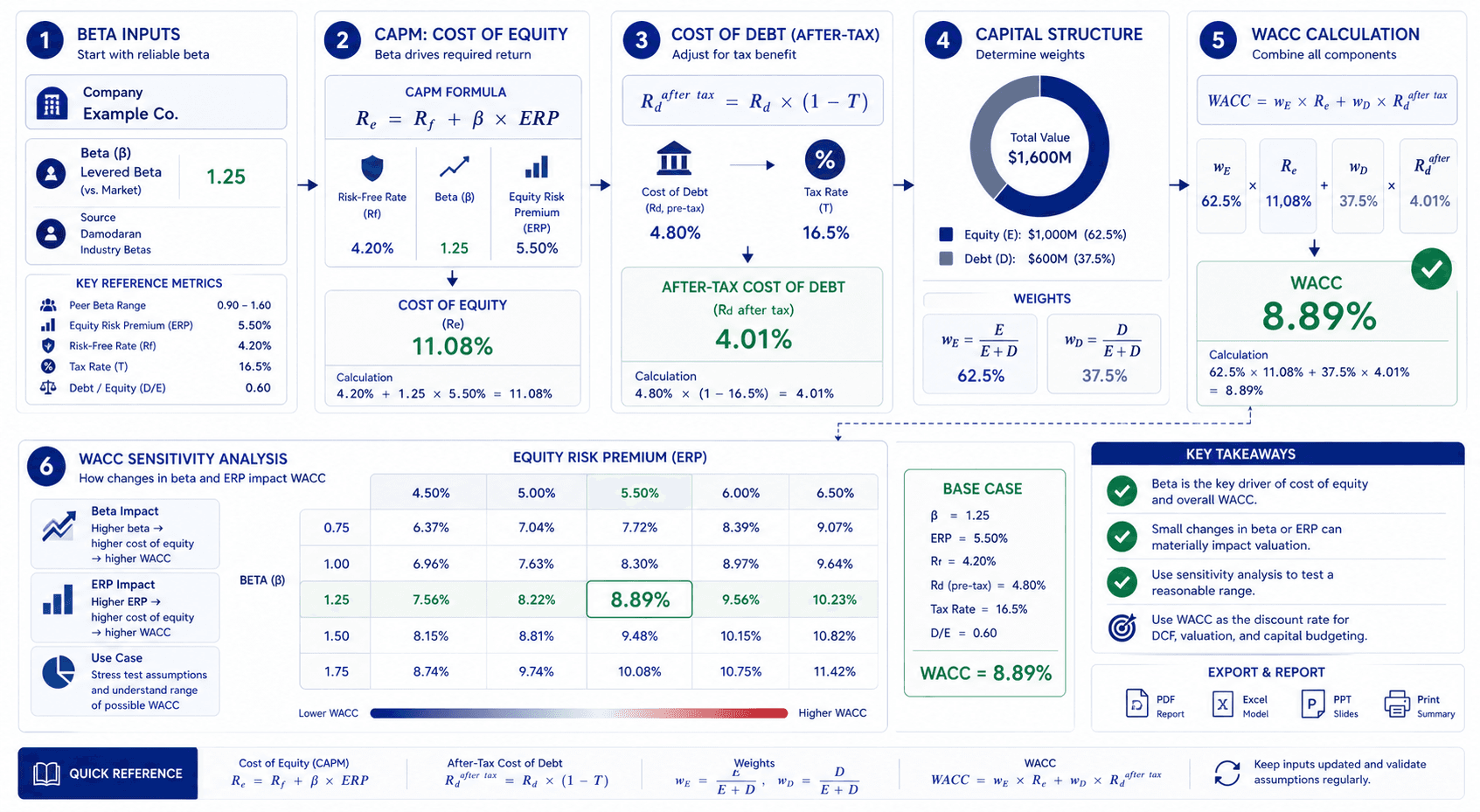

3. How to Apply Your Beta in BizToolkitPro

Once you have meticulously calculated your Bottom-Up Levered Beta, you need to seamlessly integrate it into your overarching valuation model.

Pushing Beta into the CAPM Engine

BizToolkitPro eliminates the risk of spreadsheet linking errors. Inside our valuation suite, you simply enter your newly calculated Levered Beta (e.g., 1.12) into the Equity parameters section. The engine automatically pulls the current 10-year Treasury yield for the Risk-Free Rate, applies the Equity Risk Premium, and generates your Cost of Equity.

Example Calculator Output Explained

Example WACC Calculator Output | What It Shows |

|---|---|

Input Levered Beta | The 1.12 value you calculated via the Bottom-Up method. |

Implied Cost of Equity (CAPM) | e.g., 9.8% (The return shareholders demand for that 1.12 Beta). |

Capital Weights | Synchronizes your target D/E ratio with the WACC formula. |

Final Blended WACC | The definitive discount rate for your DCF model. |

Put This Into Practice: Stop rebuilding CAPM schedules from scratch. Put your calculated Levered Beta to work instantly using our WACC Calculator — blend it with your cost of debt and download a board-ready PDF memo in minutes.

Frequently Asked Questions

Should I use 2-year or 5-year Beta?

It depends on the company's recent history. A 5-year monthly Beta is the academic standard and captures a full business cycle, smoothing out noise. However, if a company underwent a massive transformation (e.g., a major acquisition or spinning off a division) two years ago, the 5-year Beta includes irrelevant historical data.

In that case, a 2-year weekly Beta provides a more accurate reflection of current risk.

What does a Beta of 1.0 mean?

A Beta of exactly 1.0 means the stock's price moves in perfect lockstep with the broader market index (typically the S&P 500). If the market goes up 5%, the stock goes up 5%. A Beta of 1.0 means the company carries the exact average risk of the market, and its cost of equity will simply equal the Risk-Free Rate plus the standard Equity Risk Premium.

Can a company's Beta be negative?

Yes, mathematically, but it is extremely rare in corporate equities. A negative Beta implies the stock moves inversely to the market (like gold or a dedicated short ETF). If you calculate a negative Beta for a standard operating company, your regression data is likely flawed or overly constrained by a bizarre, short-term macroeconomic shock.

Why do we use the marginal tax rate when unlevering Beta?

The tax rate is used in the Hamada Equation because interest on debt is tax-deductible. This "tax shield" effectively subsidizes the cost of debt, altering the true financial risk borne by equity shareholders. You use the marginal statutory rate (typically 21% to 25% in the U.S.) because it reflects the tax savings on the next dollar of interest expense incurred.

Does Beta account for bankruptcy risk?

Only indirectly. Beta measures historical price volatility relative to the market. If a company is nearing bankruptcy, its stock price will likely swing violently, resulting in a high Beta. However, Beta is a backward-looking statistical measure; it does not possess a forward-looking predictive mechanism for default probabilities.

How often does Aswath Damodaran update his Beta tables?

Professor Damodaran updates his industry Unlevered Beta, Cost of Capital, and Equity Risk Premium datasets annually, typically releasing the new data in the first week of January based on closing prices from the end of the prior year. Institutional analysts treat this January release as a mandatory update for all baseline templates.

Put This Theory Into Practice

Run your own scenario analysis with our math-verified calculators.