WACC Calculator: Weighted Average Cost of Capital Formula

Use this WACC calculator to calculate weighted average cost of capital for DCF valuation, capital budgeting, and corporate finance models. Enter equity value, debt value, CAPM cost of equity, pre-tax cost of debt, and tax rate to get a market-value WACC result.

WACC is often used as the discount rate for unlevered free cash flow because it blends the required return from equity holders and lenders. Once you have your WACC, you can plug it directly into our DCF Calculator to estimate intrinsic enterprise value. The sections below explain the WACC formula, how to calculate WACC step by step, and how assumptions such as size premium, debt cost, and tax shield can change the result.

Have a suggestion or found a calculation discrepancy? Let us know!

How to Calculate WACC Step by Step

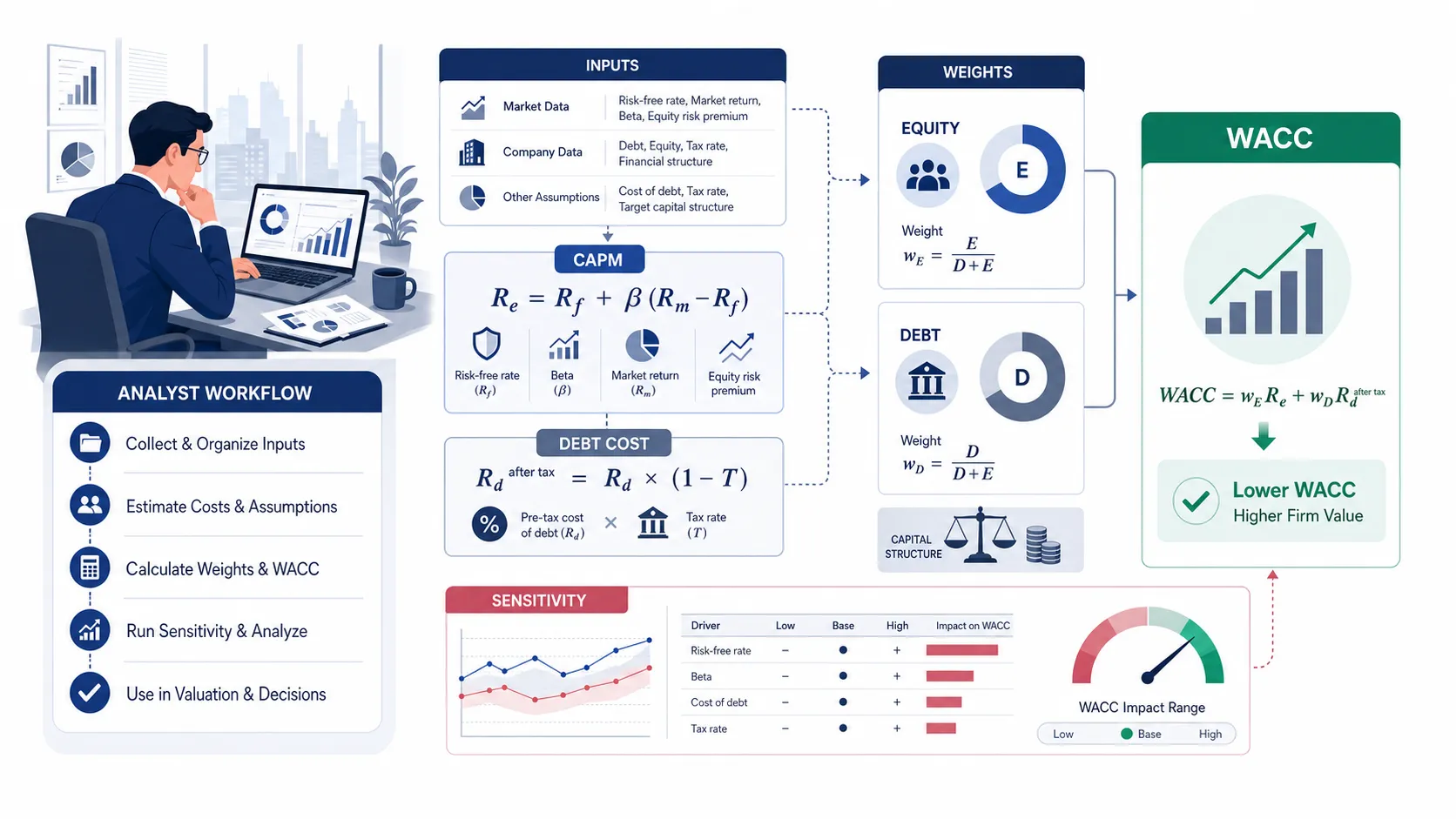

Inputs you need before calculating WACC

To run an accurate Weighted Average Cost of Capital model, you need to collect five key inputs representing the capital structure and funding costs of the business:

- Market Value of Equity (E): Typically the total shares outstanding multiplied by the current stock price.

- Market Value of Debt (D): The market value or total book value of all outstanding interest-bearing debt liabilities.

- Cost of Equity (Re): The required rate of return demanded by equity shareholders, often derived via CAPM.

- Cost of Debt (Rd): The average pre-tax interest rate paid on corporate loans, bonds, and notes.

- Corporate Tax Rate (Tc): The marginal tax rate applicable to corporate profits, used to derive the interest tax shield.

How to read the WACC result

Once computed, the calculator outputs the blended cost of capital. An equity weight (E/V) and debt weight (D/V) represent the proportions of corporate funding.

The After-tax Cost of Debt reflects the interest deduction benefit, while the final WACC percentage represents the average hurdle rate. The sensitivity grid shows how the WACC shifts as the weight of debt and the cost of equity fluctuate, and the Scenario Comparison contrasts conservative (Bear), moderate (Base), and optimistic (Bull) states.

WACC Formula

Core WACC formula

The Weighted Average Cost of Capital (WACC) represents the average rate of return a company is expected to pay to all its security holders to finance its assets. It is mathematically formulated as:

Equity and debt weight definitions

Capital structure is divided into equity and debt. The proportion of each funding source dictates its weight (E/V and D/V) in the total capital pool. In an institutional framework, these weights should always be calculated using market values rather than book values, as book values reflect historical accounting allocations rather than current market opportunities.

Cost of Equity (Re) represents the return equity investors demand for bearing the risk of stock ownership. It is commonly calculated via the Capital Asset Pricing Model (CAPM): Re = Rf + Beta * ERP, where Rf is the Risk-Free Rate, Beta represents systemic equity volatility, and ERP is the Equity Risk Premium.

After-tax cost of debt assumption

Cost of Debt (Rd) is the average rate the company pays on outstanding debts. Because debt interest is tax-deductible in most jurisdictions, the true corporate burden of debt is reduced by the tax shield. This yields the tax-adjusted cost of debt formula: After-tax Rd = Rd * (1 - Tc). This shield reduces the overall WACC, making debt financing cheaper than equity, though excessive leverage introduces financial distress risks.

Cost of Equity, Cost of Debt, and Tax Shield

Cost of equity

Cost of equity is the return equity investors require for owning the business. Analysts often estimate it with CAPM using the risk-free rate, levered beta, and equity risk premium.

Cost of debt

Cost of debt is the borrowing rate on loans, bonds, or private credit. The input should reflect the current marginal borrowing cost when the model is forward-looking.

Interest tax shield

Because interest expense may reduce taxable income, WACC uses after-tax debt cost. The formula is pre-tax cost of debt multiplied by one minus the tax rate.

Size Premium and Company-Specific Risk Premium in WACC

Private company WACC

Private companies usually do not have observable market capitalization or traded beta. Analysts often use guideline public companies, peer capital structures, normalized borrowing rates, and target leverage to estimate a defensible WACC range.

Size premium in CAPM and WACC

The size premium in CAPM adjusts cost of equity upward to reflect the higher required return demanded by investors in smaller companies. When added inside the CAPM formula — alongside the risk-free rate, beta, and equity risk premium — the size premium in CAPM captures incremental risk from customer concentration, limited access to capital markets, thinner management depth, or less liquid ownership. This size-adjusted cost of equity then flows directly into the WACC calculation.

A company-specific risk premium is distinct from a broad size premium. It should be tied to identifiable, firm-level risks such as revenue concentration, unstable margins, refinancing pressure, or dependence on a small management team. Because this input can materially raise WACC, analysts should document the rationale for each premium and test a sensitivity range instead of relying on a single point estimate.

WACC vs Discount Rate

When WACC fits

WACC is typically appropriate for unlevered DCF models where projected free cash flow belongs to all capital providers and the capital structure is reasonably stable.

When another rate fits

Project-specific, country-specific, or venture-stage cash flows may require a different discount rate if their risk profile is materially above or below the company's blended cost of capital.

Sensitivity matters

Small discount rate changes can materially change DCF value. Analysts should test WACC ranges rather than relying on a single point estimate.

WACC example calculation

Example inputs

To demonstrate WACC derivation, let's take a hypothetical mid-market firm with the following capital and rate metrics:

- Market Value of Equity (E) = $1,000,000

- Market Value of Debt (D) = $250,000

- Cost of Equity (Re) = 12.00%

- Pre-tax Cost of Debt (Rd) = 6.00%

- Corporate Tax Rate (Tc) = 21.00%

Step-by-step WACC calculation

First, sum total capital: V = $1,000,000 + $250,000 = $1,250,000.

Next, calculate the proportions: Equity Weight (E/V) = 80.00%, Debt Weight (D/V) = 20.00%.

Calculate the tax-shielded cost of debt: After-tax Rd = 6% * (1 - 0.21) = 4.74%.

Finally, blend the values: WACC = (80% * 12%) + (20% * 4.74%) = 9.60% + 0.95% = 10.55%. This 10.55% serves as the baseline discount rate.

What your WACC result means

What a higher WACC means

A higher WACC indicates that a company has a higher risk profile in the eyes of market investors. Because capital providers demand greater returns for higher risk, the cost of raising capital increases. In valuation terms, a high cost of capital dampens asset value because future cash flows are discounted heavily.

What a lower WACC means

A lower WACC suggests that corporate operations are stable and low-risk, allowing the company to raise capital cheaply. Low discount rates preserve cash flow value in DCF models, yielding higher enterprise value. Blue-chip companies with stable revenues typically enjoy lower WACCs.

How WACC affects DCF valuation

In a Discounted Cash Flow model, WACC is the denominator. A small change in the discount rate has a compounding effect over multi-year cash flow projections. For instance, increasing WACC from 9% to 10.5% in a 10-year model can trigger a double-digit percentage decline in intrinsic business valuation.

WACC use cases for startups, SaaS, and private companies

Startup WACC calculator assumptions

Early-stage startups lack public stock pricing and market volatility (Beta) indices. Furthermore, startups rarely carry traditional bank debt due to lack of hard collateral. Consequently, a startup's WACC is heavily equity-weighted, and the cost of equity is set high (often 25%-40%) to account for the elevated failure rate of venture capital investments.

SaaS WACC and DCF discount rate assumptions

SaaS models generate recurring revenue (ARR/MRR) which commands premium valuations. However, high-growth SaaS firms often operate at high burn rates. Cost of capital calculations for SaaS rely on public peers' SaaS software index Betas, typically adjusted upward to reflect growth and cash flow visibility differences.

Private company WACC without public market data

Valuing a private company requires "unlevering" and "relevering" Peer Betas. Analysts identify a group of public comparable companies, calculate their unlevered Beta to isolate operating business risk from financial structure risk, and then relever the average Beta based on the private company's specific target debt-to-equity ratio.

- Book Value weighting: Utilizing historical accounting values rather than current market capitalizations of equity.

- Pre-tax Cost of Debt: Omitting the interest tax shield deduction term

(1 - Tc). - Inflation mismatch: Mixing real (inflation-adjusted) cash flows with nominal discount rates, or vice versa.

Real-world case study: Apple Inc. (AAPL, FY 2023)

Apple Inc. metrics profile

Apple Inc. (AAPL) is a global technology leader known for its consumer electronics, software, and online services. Analyzing its Weighted Average Cost of Capital (WACC) for Fiscal Year 2023 provides insight into the company's cost of financing its assets and overall financial health, crucial for investment decisions and strategic planning.

Apple's WACC of 10.55% for FY2023 reflects its strong financial standing and relatively low-cost access to capital. The high proportion of equity in its capital structure (approximately 95.6%) means its WACC is heavily influenced by its cost of equity, which is calculated using a beta of 1.09, a risk-free rate of 4.44%, and a market risk premium of 5.94%. The low cost of debt (3.07%) further contributes to a favorable WACC, indicating efficient debt management. This robust WACC suggests that Apple can finance its growth initiatives and operations at a competitive rate, making it an attractive prospect for investors seeking stable returns from a well-managed technology giant. It demonstrates the company's ability to generate value for its shareholders by deploying capital effectively.

Learn the WACC Formula In Depth

Want a full walkthrough of the weighted average cost of capital before using the calculator? Our editorial guides cover the WACC formula, cost of equity derivation via CAPM, and real-world benchmark comparisons:

- How to Calculate WACC Step by Step — Formula, Inputs, and ExamplesA practical guide covering how to calculate WACC step by step: from collecting market-value weights to deriving after-tax cost of debt.

- Weighted Average Cost of Capital Formula — WACC Components ExplainedExplains the weighted average cost of capital formula in detail: equity weight, debt weight, CAPM cost of equity, and tax shield mechanics.

Related Calculators

Value a business using discounted cash flows.

Open Tool →NPV CalculatorCompute net present value of cash flows.

Open Tool →IRR CalculatorSolve project internal rates of return.

Open Tool →Free Cash Flow CalculatorEstimate operating free cash flow.

Open Tool →Break-Even ROI CalculatorAnalyze payback thresholds and returns.

Open Tool →EBITDA Margin CalculatorAssess earnings margin before interest and tax.

Open Tool →Related Articles & Guides

Corporate Finance

Corporate FinanceWACC by Industry: 2026 Benchmarks for Technology, Healthcare, and Real Estate

In 2026, industry WACC diverges sharply, from 5.5% for utilities to over 11.5% for software. CFOs must benchmark their discount rate against peers to ground valuations in market reality.

Corporate Finance

Corporate FinanceHow to Calculate WACC: The Complete Step-by-Step Formula for Corporate Valuation

A 100-basis-point WACC error can swing a $500M valuation by $40–80M. This guide delivers the exact formula and five critical inputs corporate operators need to get the discount rate right.

Corporate Finance

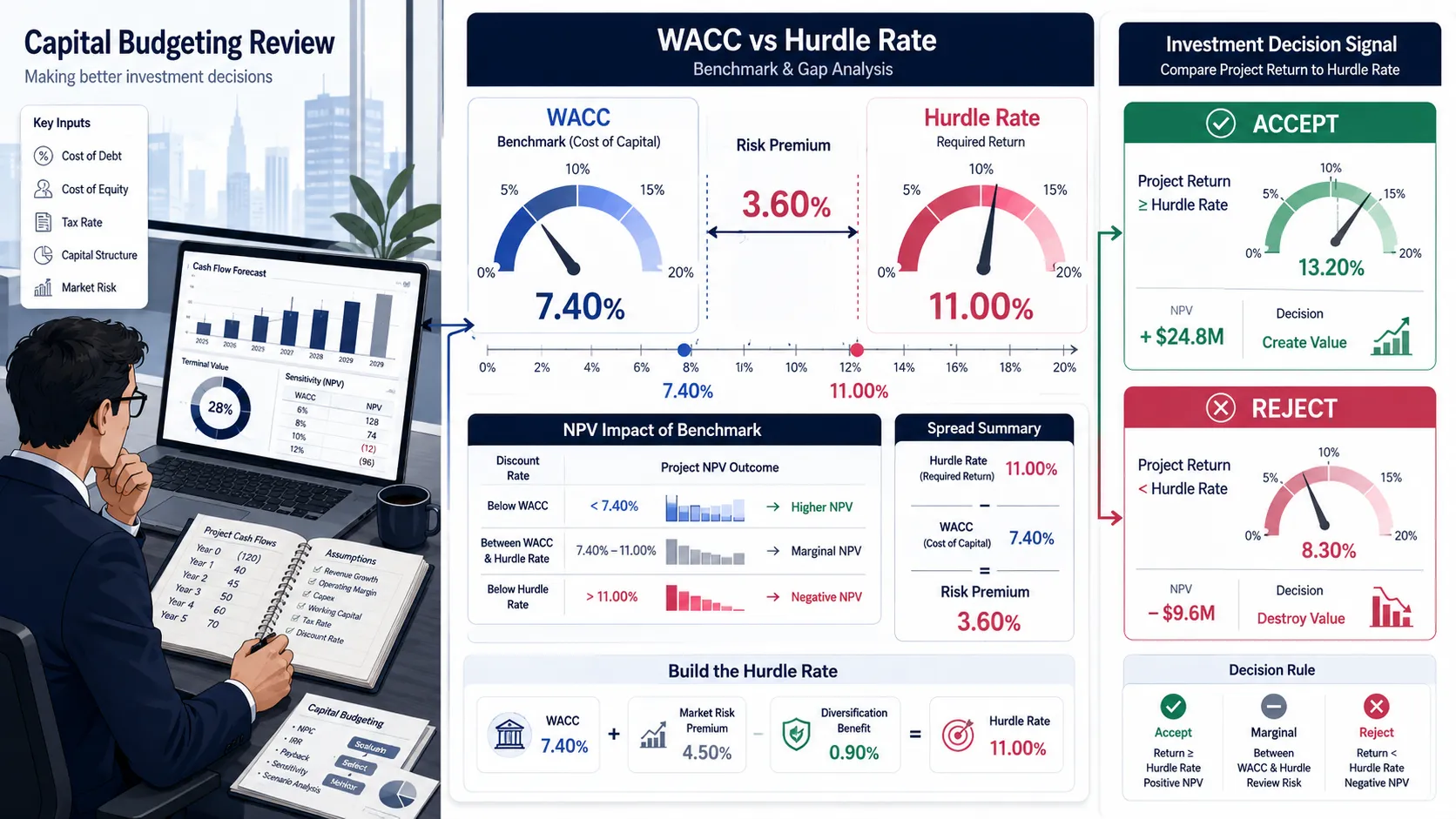

Corporate FinanceWACC vs Hurdle Rate: What's the Difference in Capital Budgeting?

WACC reflects your true cost of capital from markets, while the hurdle rate is management’s higher bar to approve projects, adding a buffer against risk and overoptimism.

Frequently Asked Questions

What is a good WACC?

Should I use book value or market value for WACC?

Why does WACC matter in a DCF model?

Can WACC be used as a discount rate?

How often should I update WACC assumptions?

The calculations, projections, and reports generated by BizToolkitPro are for educational and informational purposes only. They do not represent professional investment advice, financial planning, tax guidance, legal counsel, or formal business valuation.

Financial models and valuation formulas (including WACC, DCF, IRR, and NPV) rely on assumptions and inputs provided directly by the user. Actual financial markets and business metrics fluctuate; therefore, BizToolkitPro makes no warranties, express or implied, regarding the accuracy, completeness, or suitability of the outputs for any investment strategy or corporate decision.

Always perform your own independent diligence and consult with a licensed Financial Analyst, Certified Public Accountant (CPA), or certified valuation specialist before committing capital or executing corporate transactions.