IRR Calculator: Calculate Internal Rate of Return Step by Step

Every capital allocation decision hinges on one question: does this project return more than it costs? IRR answers that in a single annualized percentage—the breakeven return on invested capital. Get it wrong, and you risk rejecting value or funding capital destruction.

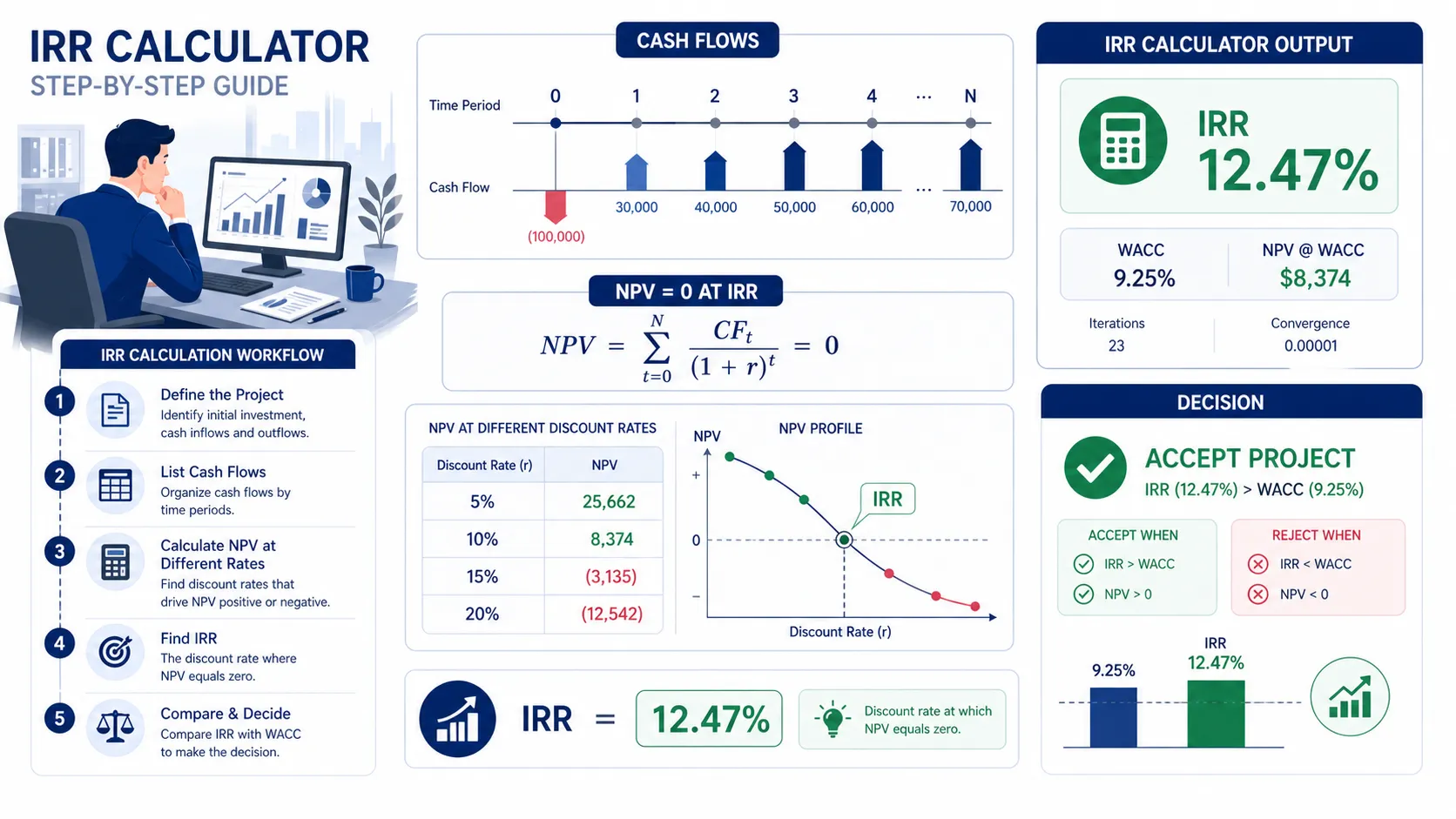

IRR is the discount rate at which a project's net present value equals exactly zero — the breakeven return on your invested capital.

NPV = 0 = CF₀ + CF₁/(1+IRR) + CF₂/(1+IRR)² + ... + CFₙ/(1+IRR)ⁿTo use an IRR calculator: enter your initial outflow (as a negative number), followed by each period's projected cash inflow. The calculator solves for IRR iteratively. Compare the result to your hurdle rate (WACC): if IRR > WACC, the project creates shareholder value.

Every capital allocation decision reduces to a single question: does this project return more than it costs? IRR answers that question in a single percentage — the annualized breakeven return rate. Get it wrong, and you will either reject value-creating projects or fund ones that destroy capital.

The IRR Formula: What It Calculates and Why Excel Gets It Wrong

Put This Theory into Practice

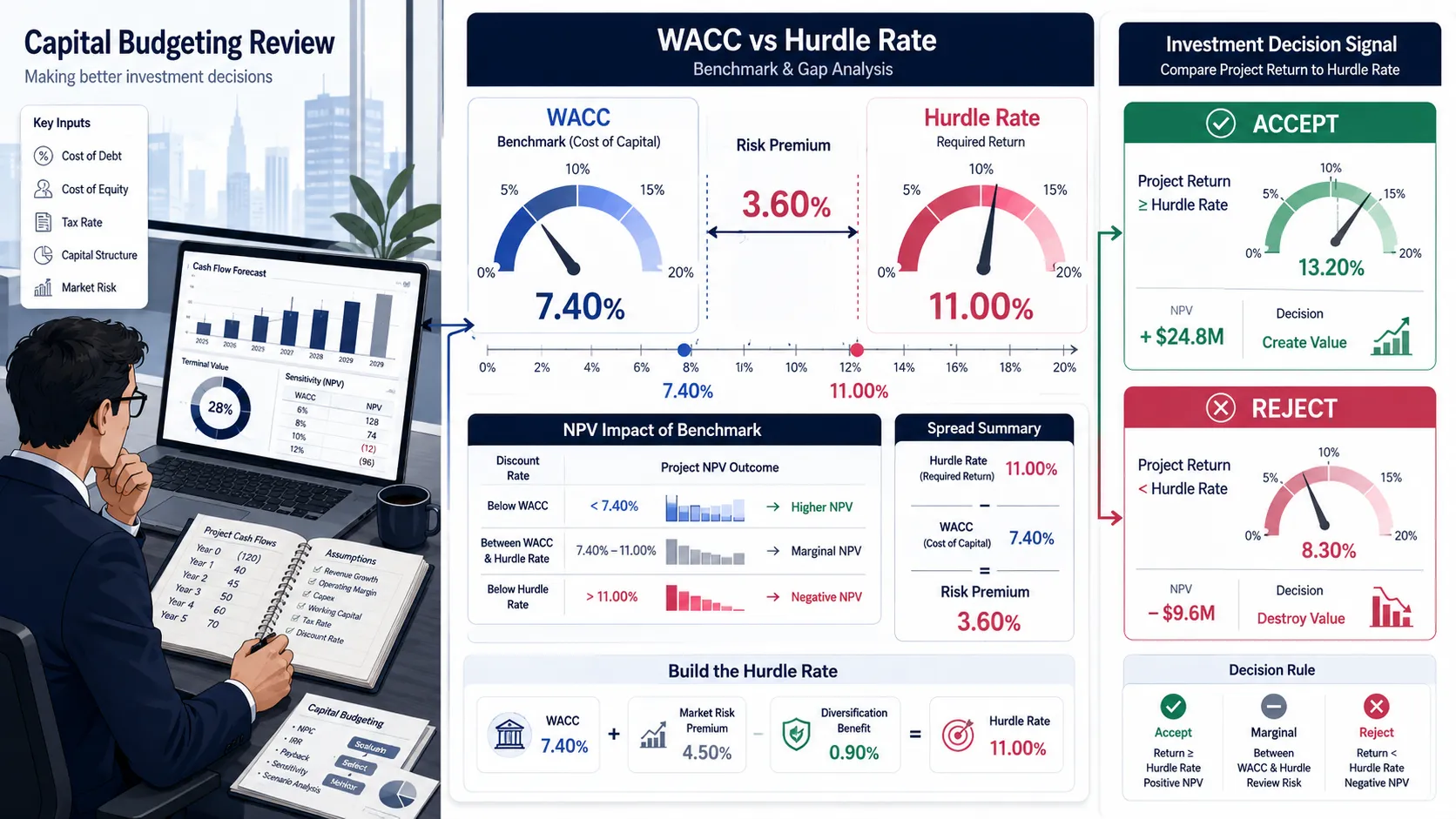

Calculate WACC step by step using market-value equity and debt weights, CAPM cost of equity, and after-tax cost of debt. Enter your own inputs to model the weighted average cost of capital for any company. Enter your custom inputs and simulate scenarios in our math-verified WACC Calculator.

IRR is not a formula you can solve directly — it is an implicit equation. The IRR is the value of r that makes the following equation true:

0 = CF₀ + CF₁/(1+r)¹ + CF₂/(1+r)² + ... + CFₙ/(1+r)ⁿ

Because no closed-form algebraic solution exists, IRR is always calculated through numerical iteration — a process that guesses, checks, and converges on the answer. This is why you need a calculator or spreadsheet function, not a manual formula.

How IRR Works: The NPV = 0 Equation

The intuition: at the IRR discount rate, the present value of all future cash inflows exactly equals the present value of all outflows. You are not earning more than your cost of capital — you are breaking even on a risk-adjusted basis.

The table below shows the standard inputs required for any IRR calculation:

Input | What It Represents | Example |

|---|---|---|

CF₀ (initial investment) | Upfront outflow, entered as a negative value | −$500,000 |

CF₁ through CFₙ (periodic cash flows) | Projected net cash inflows each period | $120K, $150K, $180K... |

Projection period (n) | Number of periods (years, quarters) | 5 years |

Hurdle rate (WACC) | Required return for comparison | 9.5% |

Terminal cash flow (if applicable) | Exit proceeds or residual value in final period | $300,000 |

A well-structured IRR analysis requires realistic cash flow forecasts, not round numbers. Stress-testing the model with a downside scenario (cash flows 20% lower) is standard practice before any investment committee presentation.

Common IRR Modeling Mistakes That Lead to Wrong Investment Decisions

IRR is one of the most misapplied metrics in corporate finance. These four errors appear most often in practice:

Ignoring the reinvestment rate assumption. IRR implicitly assumes that interim cash flows are reinvested at the IRR itself — an assumption that is rarely realistic for high-IRR projects. When this assumption matters, use Modified IRR (MIRR) instead, which lets you specify a separate reinvestment rate.

Using IRR alone to rank mutually exclusive projects. A project with a 35% IRR on a $50K investment is not automatically better than a 22% IRR project on a $2M investment. Scale matters. Always use NPV alongside IRR for project ranking — IRR measures efficiency, NPV measures value creation.

Applying IRR to non-conventional cash flows. If a project has multiple sign changes (e.g., negative → positive → negative cash flows), the IRR equation can produce multiple mathematical solutions. The result becomes uninterpretable. Use NPV or MIRR for projects with non-standard cash flow patterns.

Confusing gross IRR with net IRR. Private equity funds distinguish between gross IRR (before management fees and carried interest) and net IRR (what LP investors actually receive). These can differ by 300–500 basis points. Always clarify which basis is being quoted before comparing to a hurdle rate.

When Excel's IRR Function Breaks Down — and What to Use Instead

Excel's =IRR() function works reliably only under two conditions: cash flows occur at regular intervals, and there is exactly one sign change (one block of outflows followed by one block of inflows). Outside these conditions:

Irregular timing: Use

=XIRR(), which accepts specific dates for each cash flow rather than assuming equal periods.Multiple sign changes: Use

=MIRR()or move to a scenario-based NPV analysis instead.Sensitivity analysis: Excel requires manual data tables to stress-test IRR across changing assumptions. A purpose-built calculator generates a full sensitivity grid in seconds.

💡 Skip the iteration problem entirely. Our IRR Calculator handles XIRR timing, MIRR reinvestment rates, and sensitivity grids — enter your cash flows and get your IRR, NPV, and payback period in one view.

Step-by-Step: Using the BizToolkitPro IRR Calculator

Entering Your Cash Flow Inputs and Projection Period

The IRR Calculator accepts up to 20 cash flow periods. Here is the input workflow for a standard capital investment analysis:

Step 1 — Initial Investment: Enter the upfront outflow as a negative number (e.g., −500000 for a $500,000 investment). This is Period 0.

Step 2 — Periodic Cash Flows: Enter each year's projected net cash inflow sequentially. Include any terminal residual value (asset sale, exit proceeds) in the final period's cash flow.

Step 3 — Hurdle Rate: Enter your company's WACC or required minimum return. The calculator computes NPV simultaneously at this rate. Use our WACC Calculator if you have not yet determined your hurdle rate.

Step 4 — Select Output Mode: Choose standard IRR, MIRR (specify reinvestment rate), or XIRR (enter specific dates). Most corporate finance uses standard IRR; real estate and private equity often require XIRR.

Complete Worked Example

The following illustrative manufacturing project uses hypothetical inputs. Verify all results with the calculator before including in an investment memo.

Period | Cash Flow |

|---|---|

0 (Initial investment) | −$500,000 |

Year 1 | $120,000 |

Year 2 | $150,000 |

Year 3 | $180,000 |

Year 4 | $160,000 |

Year 5 (incl. $200K terminal residual) | $340,000 |

Running these inputs through the IRR Calculator produces:

IRR ≈ 21.7% — well above a 9.5% hurdle rate; the project creates value

NPV at 9.5% ≈ $199,000 — positive dollar value creation at the hurdle rate

Payback period ≈ 3.3 years — the initial $500K is recovered partway through Year 4

⚠️ These figures are illustrative. Run your own cash flow inputs through the IRR Calculator before committing to any decision — small changes to Year 1 revenue or terminal value can shift IRR by 3–5 percentage points.

Reading the Output: IRR, NPV, and Payback Period

Once you submit your inputs, the calculator returns a comprehensive results panel:

Example IRR Calculator Output

Output | What It Shows |

|---|---|

IRR (%) | Annualized breakeven discount rate for your cash flow series |

NPV at hurdle rate | Dollar value created at your specified WACC; positive = value-accretive |

Payback period | Periods to recover the initial investment (undiscounted) |

Discounted payback | Periods to recover investment in present value terms |

MIRR (if selected) | IRR adjusted for a realistic reinvestment rate |

Sensitivity table | IRR and NPV grid across varying initial investment and terminal value assumptions |

Interpreting the result: If your IRR is 21.7% against a 9.5% WACC, the project clears the hurdle by 1,220 basis points — a strong value-creation signal. Use the sensitivity table to confirm this conclusion holds even if Year 1 cash flows come in 20% below forecast.

For multi-project comparisons, rank by NPV (not IRR) when project scales differ. Use our NPV Calculator for a direct present-value comparison. For a DCF Calculator approach that models free cash flow growth explicitly, link WACC and IRR into a full valuation framework.

Put This Into Practice: Stop manually iterating through IRR guesses in Excel. Use our IRR Calculator to get your IRR, NPV, MIRR, payback period, and sensitivity table in under 60 seconds — with a downloadable PDF memo formatted for investment committee review.

Frequently Asked Questions

What is a good IRR for a real estate investment?

IRR benchmarks vary significantly by property type, leverage, and market cycle. As a general reference for U.S. real estate under 2026 market conditions:

Core / core-plus (institutional, low-risk): 7%–10% levered IRR

Value-add (repositioning plays): 12%–16% levered IRR

Opportunistic / development: 18%–25%+ levered IRR

These benchmarks assume stabilized exit cap rates and moderate leverage (55–65% LTV). For corporate capital expenditures, a well-run industrial company typically targets IRR ≥ 15% on growth projects. Always model IRR on an unlevered basis first, then layer in financing to isolate what capital structure contributes.

Is a higher IRR always better?

Not always — scale matters. A $100K project with a 40% IRR creates $40K of annualized return. A $10M project with an 18% IRR creates $1.8M. When choosing between mutually exclusive investments of different sizes, always compare NPV (not IRR). IRR measures return efficiency; NPV measures absolute value creation.

Additionally, very high IRRs (>40%) often signal either a very short payback window or an unrealistic reinvestment rate assumption — IRR implicitly assumes all interim cash flows are reinvested at the IRR itself. Use MIRR with a realistic reinvestment rate to test whether the IRR figure is economically defensible.

What is the difference between IRR and XIRR?

The standard =IRR() function assumes cash flows occur at perfectly equal intervals (e.g., exactly 12 months apart). =XIRR() accepts a specific date for each cash flow, making it essential whenever timing is irregular — quarterly distributions, real estate closings on specific dates, or milestone-based payments.

For most corporate capital budgeting models with annual cash flows, standard IRR is sufficient. For private equity, real estate, or any deal with irregular cash flow timing, always use XIRR. The BizToolkitPro IRR Calculator supports both modes.

Should I use IRR or NPV for project ranking?

Use NPV for ranking; use IRR for screening. When you have multiple competing projects and limited capital, NPV tells you which option creates the most dollar value — which is the correct objective for shareholders. IRR tells you which project is most capital-efficient, but it can mislead when projects differ significantly in scale or duration.

The practical workflow: screen out any project whose IRR falls below your WACC (negative NPV by definition), then rank the remaining candidates by NPV. Use our NPV Calculator for side-by-side comparisons at a consistent discount rate.

What is the difference between IRR and WACC?

WACC is the required return — the minimum rate an investment must generate to satisfy all capital providers (equity and debt holders combined). IRR is the projected return on a specific investment — the annualized rate at which that investment breaks even in present-value terms.

The decision rule: if IRR > WACC, the investment has positive NPV and creates value. If IRR < WACC, it destroys value and should be rejected. Use our WACC Calculator to establish your hurdle rate before benchmarking any project's IRR.

Can IRR be negative, and what does that mean?

Yes. A negative IRR means the project never recovers its initial investment in present-value terms — even at a 0% discount rate, cumulative cash inflows are less than the upfront outflow. It is an unambiguous rejection signal.

Negative IRRs arise from very long payback periods, front-loaded cost overruns, or revenue assumptions that fail to materialize. Before concluding a project is unviable, verify your cash flow inputs: a single sign error on the initial investment or a missed terminal residual value can flip the IRR calculation from positive to negative.

Put This Theory Into Practice

Run your own scenario analysis with our math-verified calculators.