WACC Calculator: Weighted Average Cost of Capital Formula Step by Step

A single percentage point error in your discount rate can swing enterprise value by hundreds of millions. The WACC formula provides the precise, risk-adjusted hurdle rate needed for accurate capital budgeting and DCF valuations. Master this calculation to ensure every major financial decision is grounded in defensible numbers.

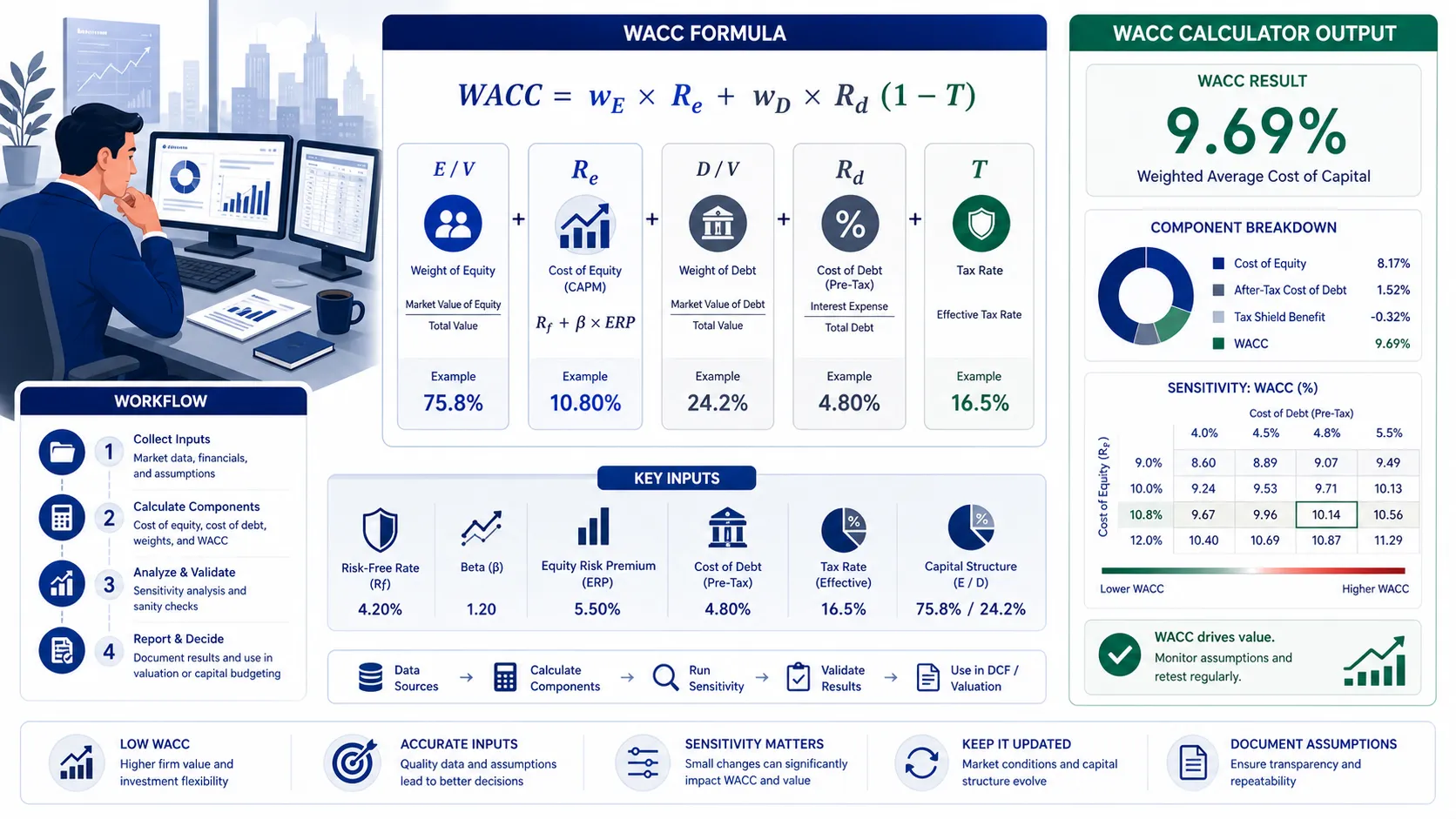

Featured Formula: Weighted Average Cost of Capital

The core formula is:

`WACC = (E/V × Re) + [D/V × Rd × (1 - T)]`It mathematically blends a company's cost of equity (calculated via CAPM) and its after-tax cost of debt based on their respective market value weights. This resulting percentage serves as the hurdle rate for capital budgeting and the primary discount rate for Enterprise DCF models.

When valuing a business or assessing the viability of a new capital project, the discount rate acts as the ultimate arbiter of value. If you miscalculate the hurdle rate by just 100 basis points, your resulting Enterprise Value could swing by hundreds of millions of dollars.

The weighted average cost of capital formula solves this by providing a unified, risk-adjusted metric that satisfies both shareholders and creditors.

Put This Theory into Practice

Determine risk-adjusted discount rates with market weights, CAPM equity cost, and tax-shielded debt. Enter your custom inputs and simulate scenarios in our math-verified WACC Calculator.

1. The Weighted Average Cost of Capital Formula: Breaking Down Every Variable

At its core, the WACC formula is a weighted average. You calculate the cost of each type of capital (equity and debt), multiply each by its proportionate weight in the total capital structure, and sum the results.

Formula Variables and Data Sources

To execute the formula WACC = (E/V × Re) + [D/V × Rd × (1 - T)], you must define the following parameters using reliable 2026 market data:

Input | Source | Example (FY2026) |

|---|---|---|

$E/V$ (Equity Weight) | Market Capitalization | 70.0% |

$Re$ (Cost of Equity) | CAPM (Risk-Free Rate + Beta × ERP) | 10.5% |

$D/V$ (Debt Weight) | Total Debt (Market Value) | 30.0% |

$Rd$ (Cost of Debt) | Yield to Maturity on outstanding bonds | 6.5% |

$T$ (Corporate Tax Rate) | Effective Tax Rate / Marginal Tax Rate | 21.0% |

Common WACC Modeling Mistakes

Even seasoned financial analysts frequently stumble on the nuances of this formula. Ensure you avoid these critical red flags:

Using Book Value Instead of Market Value: The weights ($E/V$ and $D/V$) must reflect current market prices. Using the historical book value of equity from a balance sheet fundamentally breaks the WACC calculation.

Forgetting the Tax Shield: Interest payments on debt are tax-deductible. If you fail to multiply the cost of debt by

(1 - T), you will artificially inflate the WACC.Mismatched Risk-Free Rates: Using a 3-month T-Bill for the risk-free rate in CAPM while projecting a 10-year DCF creates a duration mismatch. Always anchor to the 10-year Treasury yield.

Stale Beta Inputs: Pulling a 5-year historical Beta during a period of massive macroeconomic shift (like the 2026 rate normalization) will misprice the company's forward-looking equity risk.

The Limits and Errors of Manual Excel Modeling

Building a WACC model from scratch in Excel is standard practice, but it creates immense efficiency bottlenecks. Analysts often hardcode tax rates, break linking formulas when pulling live Treasury data, or fail to build proper dynamic sensitivity tables.

When a Managing Director asks "what happens to our valuation if the risk-free rate jumps by 50 basis points?", manually rebuilding the CAPM inputs and updating the DCF takes too long and introduces fatal spreadsheet errors.

Skip the Spreadsheet: Use BizToolkitPro's WACC Calculator to run this calculation instantly — no formula errors, no manual sensitivity tables, and instant PDF reporting.

2. Step-by-Step Guide: Using the BizToolkitPro WACC Calculator

Our tool automates the heavy lifting of the weighted average cost of capital formula, ensuring institutional-grade accuracy. Here is how to execute a valuation scenario.

Setting Inputs and Scenario Parameters

Let us run a complete numeric example for an illustrative mid-cap technology company in 2026:

Step 1: Enter Capital Structure

Market Value of Equity ($E$): $700 Million

Market Value of Debt ($D$): $300 Million

The tool automatically calculates Total Value ($V$) as $1,000M, setting $E/V$ at 70% and $D/V$ at 30%.

Step 2: Enter Cost of Equity (CAPM) Variables

Risk-Free Rate: 4.2%

Equity Beta: 1.25

Equity Risk Premium (ERP): 5.0%

Calculated $Re$ = 4.2% + (1.25 × 5.0%) = 10.45%

Step 3: Enter Debt & Tax Variables

Pre-tax Cost of Debt ($Rd$): 6.0%

Effective Corporate Tax Rate ($T$): 25%

Calculated After-tax Debt Cost = 6.0% × (1 - 0.25) = 4.5%

Final WACC Calculation:

WACC = (0.70 × 10.45%) + (0.30 × 4.50%) = 7.315% + 1.350% = 8.665%

Interpreting the Output and Sensitivity Matrix

Once the inputs are set, the calculator generates a comprehensive breakdown. Here is how to read the output:

Example WACC Calculator Output | What It Shows |

|---|---|

Cost of Equity (CAPM) | The return demanded by shareholders for taking on equity risk (10.45%). |

After-Tax Cost of Debt | The true, tax-shielded cost of borrowing (4.50%). |

Capital Weights | The exact percentage mix of Equity (70%) and Debt (30%). |

Final Blended WACC | The definitive discount rate (8.67%) to be used in your DCF Calculator. |

Sensitivity Matrix | Shows how WACC changes if Beta shifts by ±0.2 or if interest rates shift by ±1%. |

Frequently Asked Questions

How do I find the market value of debt for the WACC formula?

While the market value of equity is easily calculated (Share Price × Outstanding Shares), publicly traded debt can be illiquid. In practice, analysts often use the book value of debt from the most recent 10-Q as a proxy for market value, provided the company is financially healthy and interest rates haven't violently swung since issuance.

Does WACC include preferred stock?

Yes. If a company has preferred stock, the formula expands: WACC = (E/V × Re) + (D/V × Rd × [1-T]) + (P/V × Rp). The cost of preferred stock ($Rp$) is simply the preferred dividend divided by the current preferred share price. Preferred dividends are not tax-deductible.

What is the optimal capital structure for minimizing WACC?

The optimal capital structure is the specific mix of debt and equity that mathematically minimizes the WACC, thereby maximizing enterprise value. Because debt is cheaper and tax-shielded, adding debt initially lowers WACC. However, taking on too much debt increases bankruptcy risk, causing both $Rd$ and $Re$ to spike, eventually pushing the WACC back up in a U-shaped curve.

Why do we multiply the cost of debt by (1 - Tax Rate)?

In the United States and most developed economies, interest payments on corporate debt are tax-deductible expenses. This creates a "tax shield." If a company pays 6% interest on its bonds but has a 25% tax rate, the government is effectively subsidizing a quarter of the interest cost, making the true, out-of-pocket cost of debt only 4.5%.

Can the weighted average cost of capital formula yield a negative number?

No. Investors always demand a positive return for taking on risk. Both the cost of equity and the cost of debt will always be positive numbers. Consequently, their weighted average must also be a positive number. A negative WACC is mathematically and financially impossible.

How often should WACC be recalculated in 2026?

WACC is a dynamic, point-in-time metric. It should be recalculated anytime a company issues new debt, conducts a massive share buyback (which alters capital weights), or when there is a fundamental macroeconomic shift in the risk-free rate or equity risk premium. For ongoing DCF maintenance, analysts typically update the WACC quarterly alongside earnings releases.

Put This Theory Into Practice

Run your own scenario analysis with our math-verified calculators.