Terminal Growth Rate Calculator for DCF Models

Use this terminal growth rate calculator to estimate the perpetual growth rate (g) for Discounted Cash Flow (DCF) valuation models. In a Gordon Growth terminal value model, small changes to terminal growth can materially change enterprise value because the assumption affects every cash flow beyond the explicit forecast period.

This online tool computes terminal growth using two standard financial methodologies: Macroeconomic Blend (weighting long-term real GDP growth and expected inflation targets) and Fundamental Reinvestment (utilizing corporate reinvestment rates and ROIC benchmarks). Ensure your steady-state models reflect reasonable economic boundaries rather than mathematical distortions.

How to use this terminal growth rate calculator

Inputs required for long-term growth estimation

To run a precise terminal growth valuation model, select your preferred methodology and compile the following parameters:

- Macro Blend mode: Enter expected long-term Real GDP growth and baseline inflation targets. Google, IMF, or central bank data typically provide these estimates.

- Fundamental Reinvestment mode: Collect the corporate reinvestment rate (reinvestment capital divided by operating income) and Return on Invested Capital (ROIC).

By aligning these inputs with actual corporate metrics, analysts can determine whether a company's terminal trajectory matches its historical capital efficiency or conforms to broader economic output limitations.

Reading the steady-state growth output

The calculator blends your parameters to derive a perpetual growth ceiling. In Macro mode, it averages long-term GDP and CPI targets. In Fundamental mode, it computes growth as the reinvestment rate multiplied by ROIC.

If the calculated rate exceeds 5.00%, the system applies a standard corporate finance cap. In long-term economics, a company cannot grow faster than the aggregate economy forever; exceeding this ceiling causes mathematical divergence in DCF denominators.

We recommend utilizing the sensitivity matrix to observe how small changes in reinvestment rates shift the implied steady-state growth rate, providing a range of realistic scenarios for financial planning.

Methodology and mathematical equations

Perpetual growth equations

We apply two standard methods to calculate the steady-state perpetual rate:

Why GDP and Inflation act as ceilings

In corporate valuation, a firm enters the "steady state" after the explicit projection period (typically 5 to 10 years). The Terminal Growth Rate (g) dictates its trajectory from year 11 into infinity.

If a company's terminal growth rate is modeled higher than the long-term nominal growth of the economy (Real GDP + Inflation), the model mathematically assumes the firm will eventually outgrow the entire country. Standard investment practice limits perpetual growth to the long-term risk-free yield or inflation targets (typically 2% to 3.5%).

Furthermore, the fundamental model ties the terminal growth to the company's internal efficiency. A firm cannot grow without investing back into its business. The equation g = Reinvestment Rate * ROIC shows that growth is a function of how much cash is retained and the return generated on that capital, creating a logical framework that prevents arbitrary growth assumptions.

Step-by-step example calculation

Example inputs

Let's analyze a stable packaging manufacturer with the following fundamental capital allocations:

- Expected long-term Return on Invested Capital (ROIC) = 12.00%

- Net Reinvestment Rate (RR) = 25.00%

- Expected macro Real GDP growth = 2.50% | Inflation target = 2.00%

Calculated growth options

Fundamental Reinvestment:g = Reinvestment Rate * ROIC = 25% * 12% = 3.00%.

Macroeconomic Blend:g = (2.5% + 2.0%) / 2 = 2.25%.

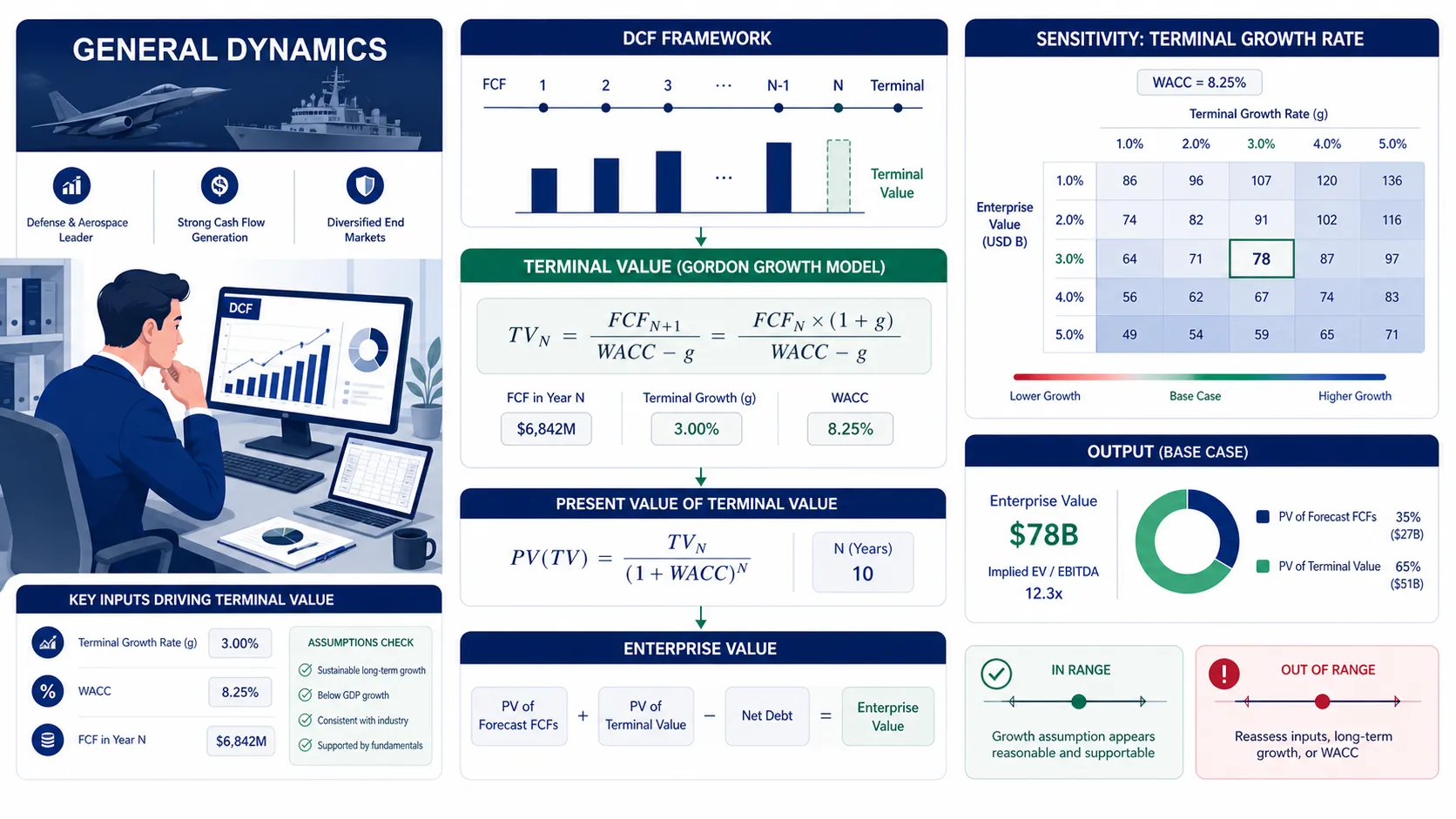

Both rates are economically sound, falling beneath the 4% global limit, and can be applied as WACC discount denominators in Gordon Growth terminal value models. Selecting the 3.00% rate implies the firm will continue to find moderately productive investment opportunities, whereas the 2.25% rate represents a more conservative steady-state economic baseline.

Strategic valuation guidelines and common mistakes

Setting g above the discount rate (WACC)

Setting a perpetual growth rate (g) higher than or equal to the Weighted Average Cost of Capital (WACC) is a fatal modeling mistake. This results in a negative denominator in the Gordon Growth equation: PV = CF / (WACC - g), causing calculation collapse and rendering the valuation meaningless.

Mistaking short-term growth for terminal growth

High-growth startups often register annual revenues expanding at 30% to 50%. This growth is temporary. Assuming a firm can maintain high double-digit expansion indefinitely yields absurd, distorted valuations. For the terminal value, always transition growth to stable inflation rates.

Ignoring capital reinvestment limitations

A firm cannot grow long-term without reinvesting a portion of its cash flow. Under the fundamental method, assuming a 0% reinvestment rate but a positive terminal growth rate represents an economic contradiction. Ensure reinvestment rates support growth assumptions.

Real-world case study: Airbnb, Inc. (ABNB, FY 2025)

Airbnb metrics profile

Analysis of Airbnb perpetual growth rate

Airbnb (ABNB) operates an asset-light online marketplace matching lodging hosts and travelers. Because the company does not own physical real estate and incurs minimal maintenance capital expenditures compared to traditional hotel chains, its Return on Invested Capital (ROIC) is exceptionally high at 22.50%.

When applying the fundamental growth formula: g = Reinvestment Rate * ROIC, a 28% net reinvestment rate yields an implied growth rate of 6.30%. While this 6.30% is mathematically consistent for the medium term, utilizing it as a perpetual terminal rate in a DCF model would be a critical planning error.

Under stable growth conditions, no corporation can outpace the nominal growth of its host economy indefinitely. Standard valuation theory requires that the terminal growth rate (g) be capped at the long-term GDP growth rate or the yield on 10-year government bonds. Therefore, when discounting Airbnb's cash flows into perpetuity, analysts should adjust the terminal rate down to a steady-state hurdle limit of 2.50% to 3.00% to ensure model convergence and prevent value distortion.

Related Calculators

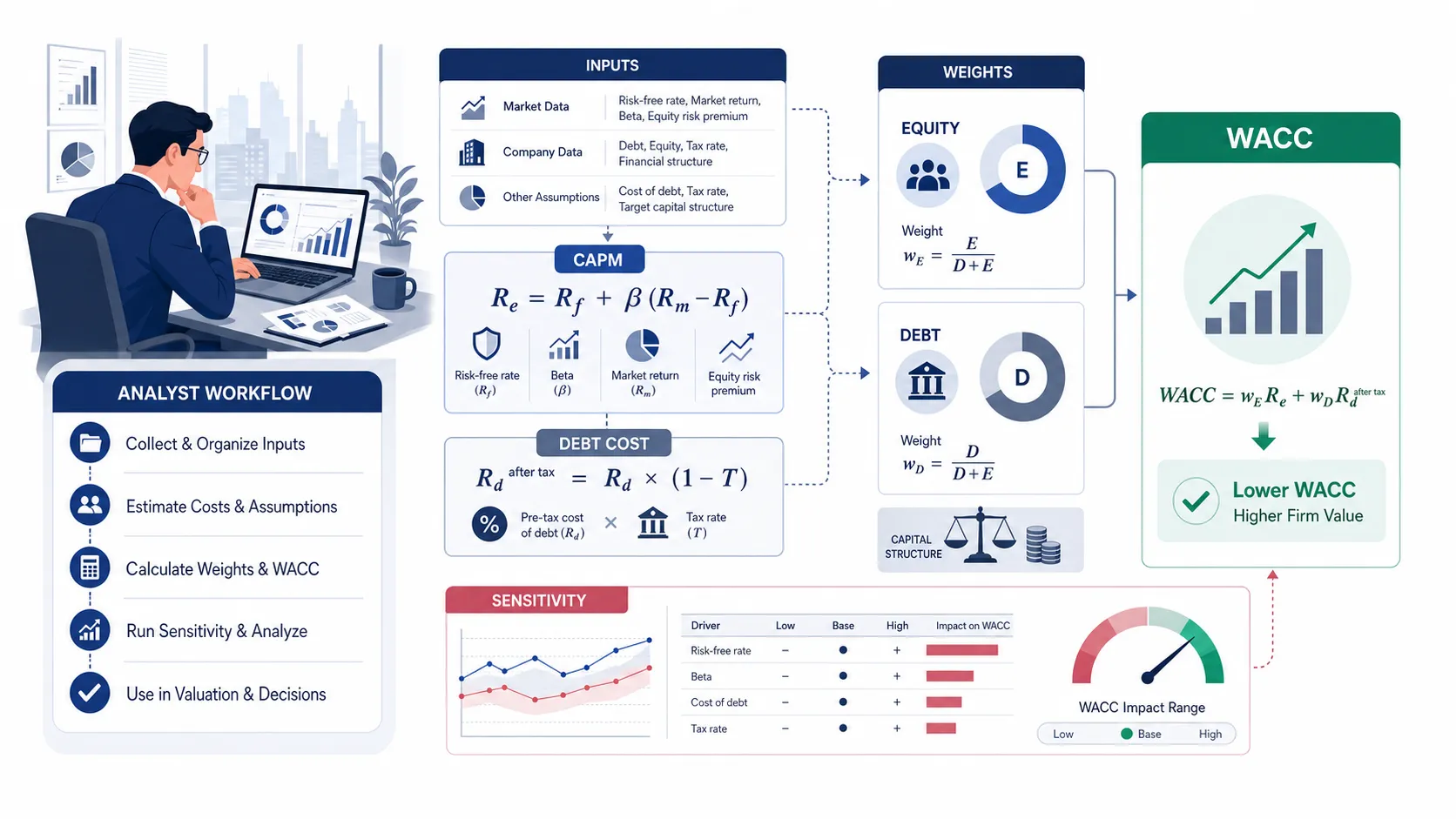

Estimate weighted average cost of capital.

Open Tool →DCF CalculatorValue a business using discounted cash flows.

Open Tool →NPV CalculatorCompute net present value of cash flows.

Open Tool →IRR CalculatorSolve project internal rates of return.

Open Tool →Free Cash Flow CalculatorEstimate operating free cash flow.

Open Tool →Break-Even ROI CalculatorAnalyze payback thresholds and returns.

Open Tool →Related Articles & Guides

Corporate Finance

Corporate FinanceTerminal Growth Rate Changes: How They Impact DCF Valuation Models

A 0.5% shift in terminal growth rate can swing DCF valuation by 15%, as terminal value often drives over 70% of enterprise worth. CFOs must cap perpetuity growth at GDP or risk-free rates to avoid model distortions.

Corporate Finance

Corporate FinanceHow to Calculate WACC: The Complete Step-by-Step Formula for Corporate Valuation

A 100-basis-point WACC error can swing a $500M valuation by $40–80M. This guide delivers the exact formula and five critical inputs corporate operators need to get the discount rate right.

Corporate Finance

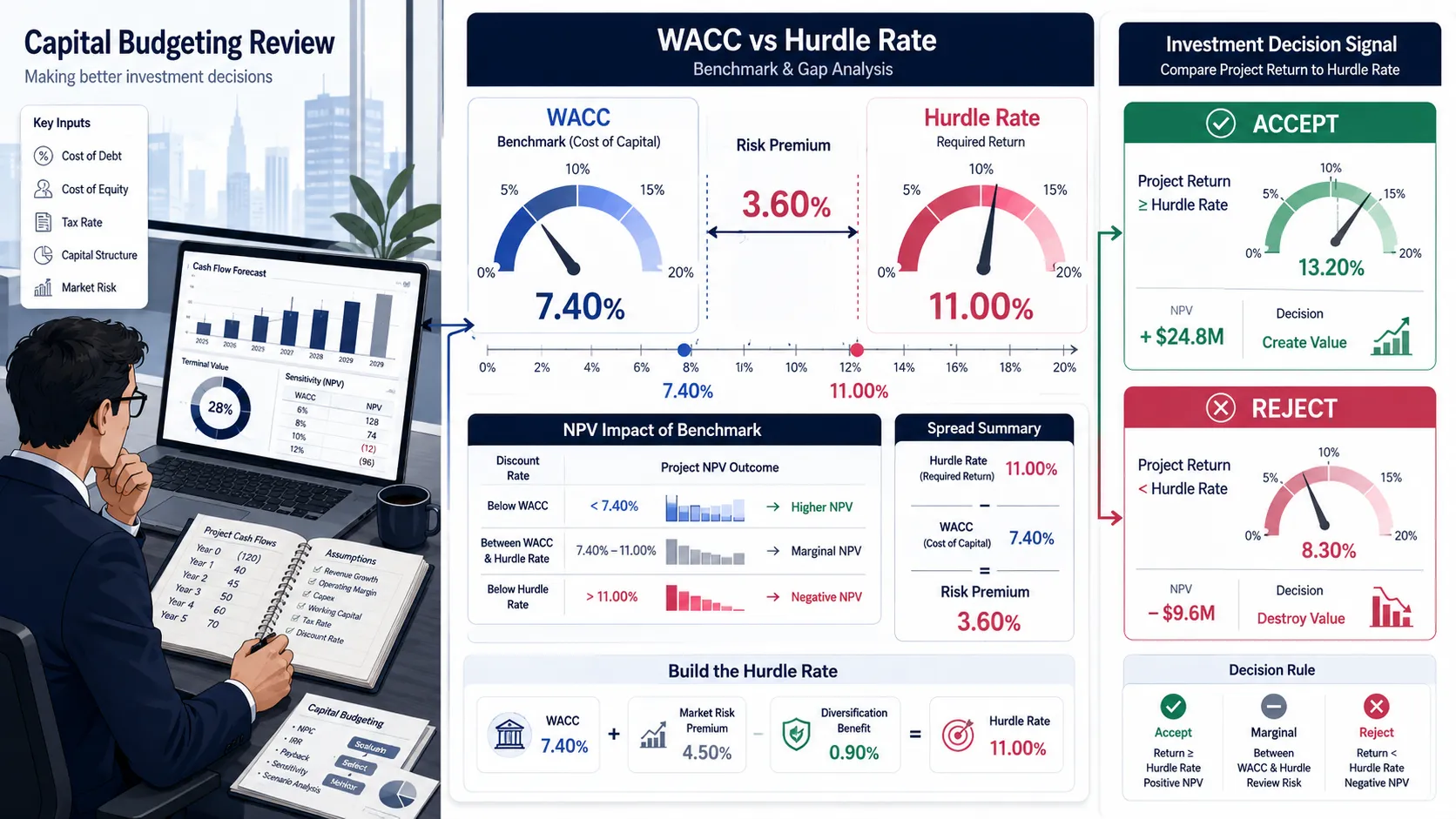

Corporate FinanceWACC vs Hurdle Rate: What's the Difference in Capital Budgeting?

WACC reflects your true cost of capital from markets, while the hurdle rate is management’s higher bar to approve projects, adding a buffer against risk and overoptimism.

Frequently Asked Questions (FAQ)

What is a reasonable terminal growth rate in a DCF model?↓

Can the terminal growth rate be negative?↓

How does terminal growth relate to Terminal Value?↓

TV = FCF_n * (1 + g) / (WACC - g). This TV represents the present value of all cash flows beyond the forecast period.How do I choose between perpetual growth and exit multiples?↓

The calculations, projections, and reports generated by BizToolkitPro are for educational and informational purposes only. They do not represent professional investment advice, financial planning, tax guidance, legal counsel, or formal business valuation.

Financial models and valuation formulas (including WACC, DCF, IRR, and NPV) rely on assumptions and inputs provided directly by the user. Actual financial markets and business metrics fluctuate; therefore, BizToolkitPro makes no warranties, express or implied, regarding the accuracy, completeness, or suitability of the outputs for any investment strategy or corporate decision.

Always perform your own independent diligence and consult with a licensed Financial Analyst, Certified Public Accountant (CPA), or certified valuation specialist before committing capital or executing corporate transactions.