What Is a Good WACC? Industry Benchmarks and Red Flags

A good WACC is accurate, not low. Most U.S. public companies range from 6% to 12% in 2026, but benchmarks vary by industry and capital structure. The real test is whether your ROIC and project IRRs consistently exceed your WACC.

The short answer is: a good WACC is an accurate WACC, not necessarily a low WACC.

Most U.S. public companies fall between 6% and 12% in 2026, but the right benchmark depends on industry, capital structure, beta, debt capacity, and the current interest rate environment. Utilities and consumer staples often sit near the lower end, while technology, biotech, and early-stage companies usually require higher WACC assumptions.

The real test is whether your company's ROIC and project IRRs consistently exceed WACC.

Defining 'Good': What WACC Benchmarks Actually Signal

Put This Theory into Practice

Calculate WACC step by step using market-value equity and debt weights, CAPM cost of equity, and after-tax cost of debt. Enter your own inputs to model the weighted average cost of capital for any company. Enter your custom inputs and simulate scenarios in our math-verified WACC Calculator.

The short answer is: a good WACC is an accurate WACC. A number that precisely reflects your company's blended required return is far more valuable than one that happens to be "low" but is built on faulty inputs. That said, industry benchmarks give you a sanity check — if your calculated WACC is wildly outside the sector median, something in your inputs deserves scrutiny.

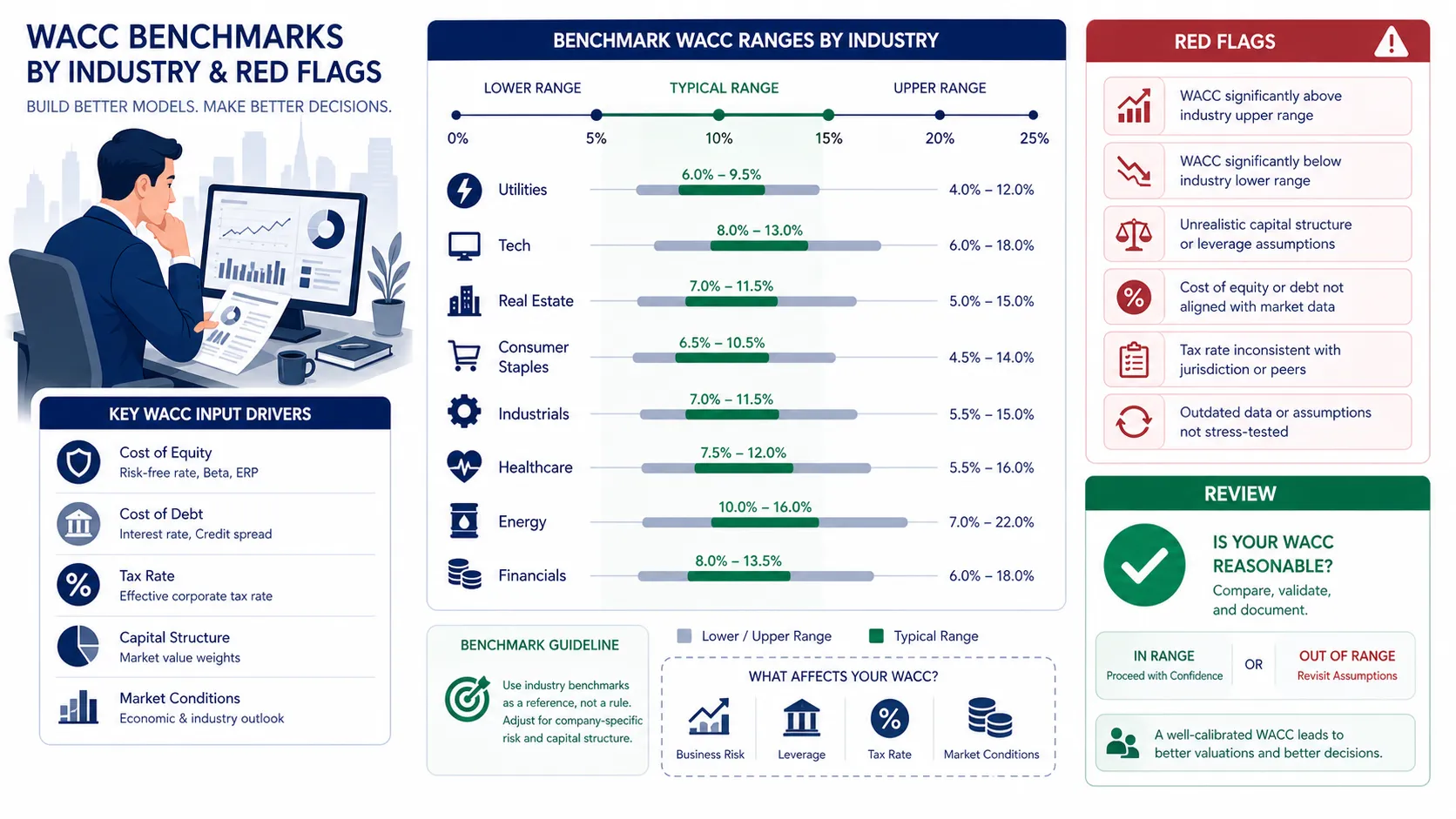

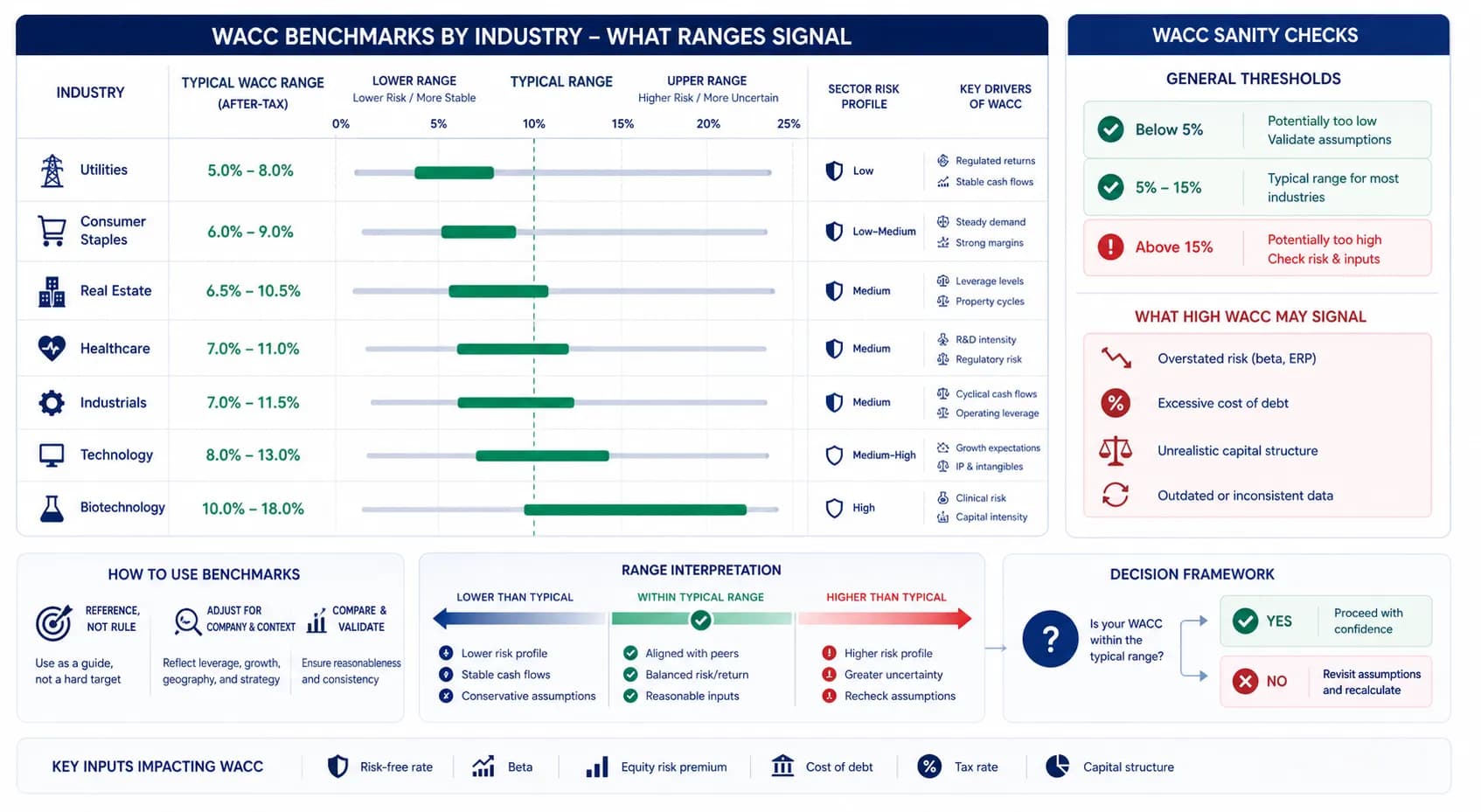

WACC by Industry: 2026 Reference Ranges for U.S. Public Companies

The ranges below are derived from Professor Aswath Damodaran's 2026 industry-level cost of capital dataset, published at his NYU Stern data page, combined with prevailing 2026 market parameters (10-year Treasury: ~4.3%, implied ERP: ~5.0%).

Industry | Typical WACC Range | What the Range Usually Signals |

|---|---|---|

Utilities | 5.5%–7.5% | Regulated cash flows, low beta, high debt capacity |

Consumer staples | 6.5%–8.5% | Stable demand, moderate leverage, defensive revenue |

Real estate / REITs | 7.0%–9.5% | Interest-rate sensitivity, asset-backed leverage |

Healthcare / pharma | 8.0%–10.5% | Regulatory risk balanced by strong cash generation |

Industrials | 8.5%–11.0% | Cyclical revenue, moderate operating leverage |

Technology | 9.0%–12.0% | Higher beta, equity-heavy balance sheets, growth risk |

Biotech / early-stage healthcare | 12.0%–18.0%+ | Binary outcomes, limited debt capacity, high risk |

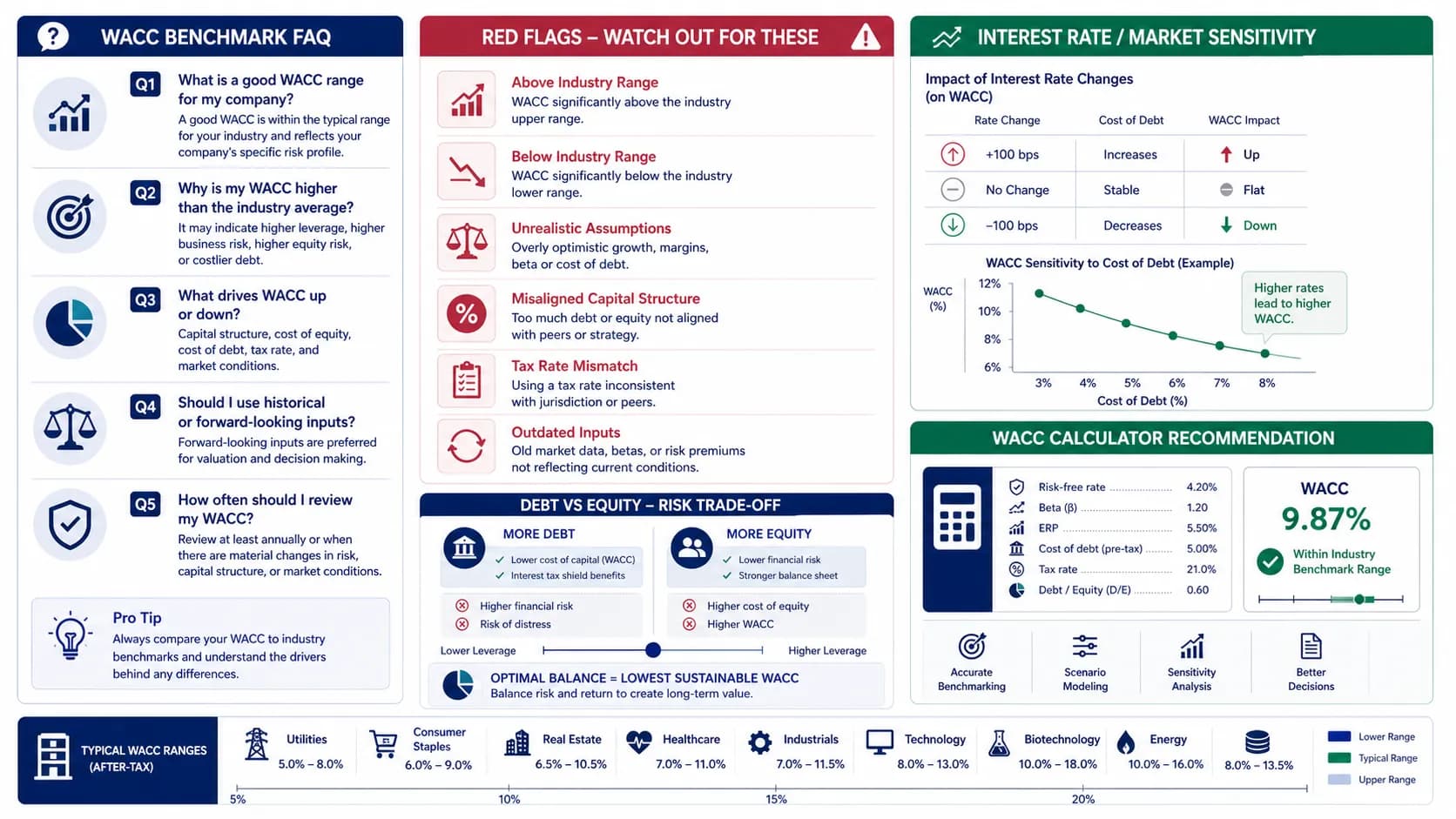

If your calculated WACC sits more than 200 basis points outside the typical range for your sector, do not automatically assume the company is unusual. First check whether your beta, ERP, debt cost, tax rate, or market-value capital structure weights are wrong.

Benchmark Your WACC Before Using It in a DCF: Use our WACC Calculator to enter your beta, ERP, debt cost, tax rate, and capital structure. The calculator returns your company-specific WACC, shows how it compares to typical industry ranges, and generates a sensitivity table for DCF scenarios.

Why a Lower WACC Is Not Always Better

The instinct to minimize WACC is understandable — a lower discount rate produces a higher present value for the same cash flows, making projects look more attractive. But this logic breaks down in three ways:

Understating WACC creates value illusions. If your true cost of capital is 10% but you model at 7%, you will approve projects that actually destroy shareholder value. This is the core risk of sloppy input sourcing.

Excessive leverage lowers WACC — until it doesn't. Adding debt reduces the weighted average cost because debt is cheaper than equity (pre-tax). But beyond a certain leverage threshold, financial distress risk increases the cost of both debt and equity, ultimately pushing WACC higher. There is an optimal capital structure, not an infinitely declining one.

Sector-low WACC does not mean sector-best business. A utility at 6.5% WACC and a tech platform at 10.5% WACC can both be excellent businesses for investors — the WACC simply reflects different risk profiles. The quality metric is whether returns on invested capital (ROIC) consistently exceed WACC, not whether WACC is low in absolute terms.

WACC Red Flag Checklist: When Your Number Needs Review

Use this checklist before relying on a WACC assumption in a DCF model or investment memo:

Red Flag | Why It Matters |

|---|---|

WACC is below 5% for a non-regulated company | The beta, ERP, or debt cost may be understated |

WACC is above 15% for a mature public company | The beta may be stale, levered incorrectly, or based on a volatile lookback period |

Debt weight is based on book value equity | WACC should use market value weights; book value significantly underweights equity in asset-light businesses |

Risk-free rate uses a 3-month T-bill | Long-duration DCF models require a 10-year Treasury reference to match cash flow duration |

Cost of debt uses historical coupon rate only | Current yield-to-maturity or refinancing cost may be materially different from the coupon on legacy bonds |

Tax rate mixes effective and marginal rates | Historical analysis uses effective rate; forward-looking models use marginal rate — never blend both |

WACC is reused from last year's model | Rate changes, beta changes, and capital structure shifts can make a one-year-old WACC materially stale |

Frequently Asked Questions

Is a WACC above 15% a red flag?

Not necessarily — context matters. For a large-cap investment-grade company, a WACC above 15% is unusual and likely signals a calculation error (stale beta, mismatched risk-free rate, or book-value equity weights). For an early-stage biotech or a highly leveraged special-situation company, 15%+ may accurately reflect the risk profile.

The diagnostic check: compare your WACC to the sector median. If you are more than 400–500 basis points above the industry average with no clear justification (recent credit downgrade, extreme leverage, binary event risk), revisit your inputs before using the number in an investment decision.

Is a lower WACC always better?

No. A lower WACC only helps if it reflects the company's true risk profile. If the rate is artificially low because the model uses stale beta, book-value weights, or an outdated cost of debt, the DCF will overstate value and may approve projects that destroy capital.

A low WACC is healthy when it comes from stable cash flows, strong credit quality, and efficient capital structure. It is dangerous when it comes from bad inputs.

What is a bad WACC?

A bad WACC is not simply a high WACC — it is one that misprices risk. A 6% WACC may be reasonable for a regulated utility but unrealistic for an early-stage software company. A 14% WACC may be excessive for a mature consumer staples company but reasonable for biotech or special-situation investing.

The best diagnostic is sector comparison. If your WACC is far outside the industry range, check the inputs before using it in a valuation model. A wrong WACC of even 150 basis points can shift a DCF enterprise value by 15–25% for a long-duration growth business.

Why does WACC decrease when a company takes on more debt?

Debt is cheaper than equity for two structural reasons: debt holders accept less risk (they have priority in bankruptcy), and interest payments are tax-deductible (the interest tax shield reduces the effective after-tax cost of debt). When a company shifts its capital structure from 100% equity toward a mix of equity and cheaper debt, the blended cost — WACC — decreases, all else equal.

The key qualifier is "all else equal." In practice, adding debt increases financial risk, which raises the required return on equity (Re goes up via higher beta). The Modigliani-Miller framework with taxes shows that the optimal capital structure maximizes the debt tax shield without triggering unacceptable distress costs. Beyond that optimal point, WACC starts rising again.

How do rising interest rates affect WACC?

Rising rates push WACC higher through two channels simultaneously:

Channel 1 — Risk-free rate. The risk-free rate (Rf) is the baseline in the CAPM cost of equity formula: Re = Rf + β × ERP. When the 10-year Treasury yield rises from 3.5% to 4.5%, cost of equity increases by approximately 100 basis points for any beta greater than zero.

Channel 2 — Cost of debt. Corporate bond yields track Treasury yields with a spread. When Treasuries rise, a company's pre-tax cost of debt (Rd) rises in parallel. Even after the tax shield, after-tax debt cost increases — which directly lifts WACC.

The 2022–2023 rate cycle illustrates this precisely. As the Fed raised rates from near-zero to 5.25%, WACCs across most U.S. sectors rose by 150–300 basis points, compressing DCF valuations by 20–40% for long-duration growth assets. This is why monitoring the 10-year Treasury yield from FRED is a core part of any ongoing valuation process.

What WACC should I use for a DCF model?

For an unlevered DCF model, use a company-specific WACC based on market value capital structure, current risk-free rate, appropriate beta, equity risk premium, pre-tax cost of debt, and effective tax rate. Do not use an industry average blindly unless you are building a rough screening model.

For final valuation work, run at least three cases: base WACC, WACC + 1.0%, and WACC − 1.0%. Small WACC changes create large valuation swings for long-duration growth companies — a 1% WACC increase can reduce enterprise value by 10–20% for a high-growth tech business with a 10-year explicit forecast period. Use our DCF Calculator to model all three scenarios side by side.

Put This Theory Into Practice

Run your own scenario analysis with our math-verified calculators.